Brian Greenberg

CEO / Founder & Licensed Insurance Agent

Brian is the founder and CEO of Insurancy and carries Life, Health, and Property & Casualty licenses in all 50 U.S. states. Since 2013, Brian has been a member of Million Dollar Round Table, a designation for the top 1% of financial advisors worldwide. Brian has been featured in Yahoo! Finance, Money.com, Entrepreneur.com, Life Happens, Forbes, MSN, and Good Financial Cents. Brian’s goal is to show customers the best products, the quickest answers to their questions, and provide expert advice.

Articles by Brian Greenberg (262)

Life Insurance Industry Trends Survey 2022 - Results

Insurancy's life insurance industry trends survey found consumers cool on insurtech: 77% reject fluctuating premiums tied to physicals, 62% are uneasy about AI in the buying process, only 7% would share DNA data, and 78% still prefer buying from a local agent. Gen Z stands apart, ranking retailers like Costco and Amazon above online agencies.

14 Steps to Settle Debt With a Creditor or Debt Collector

Overdue debt causes real stress, and calls from debt collectors can feel overwhelming. Attorney Lyle Solomon walks through 14 practical steps for settling debt with a creditor or collector: keep a collections log, validate the debt before paying, get every agreement in writing, and know the FDCPA protections that limit what collectors can do.

End of Life: A Grief Support Resource Guide

There is nothing in life harder than the death of a loved one. Grief is real, with both mental and physical symptoms, and even the very worst grief is survivable. This resource guide collects vetted links for coping with grief day to day, recognizing complicated grief, finding support groups, and supporting children and families through specific kinds of loss.

Health Resources for End-of-Life Care

End of life looks different for everyone, which makes planning ahead feel uncertain. This guide collects trusted resources for every stage: elder care and healthy aging, hospice and palliative care, advance directives, locating life insurance policies and filing claims, and grief support for the whole family.

Breast Cancer Statistics - Key Facts and Survival Rates

The American Cancer Society estimates 316,950 new invasive breast cancer cases and 42,170 deaths among US women in 2025. Median age at diagnosis is 62, incidence has risen about 1% per year from 2012 to 2021, and death rates continue a long decline thanks to screening and better treatment.

Buyer Trust and Influence Study 2024 - Key Findings

Insurancy asked nearly 2,400 US respondents about their online browsing and purchasing habits to understand what builds buying trust. The study covers how reviews, social proof, search behavior, and brand reputation shape the modern path to purchase.

COVID-19 and Life Insurance Survey - Consumer Outlook

Insurancy's COVID-19 and life insurance survey of 1,500 people found nearly half already had a policy and about 70% said the pandemic did not change their outlook on coverage. Insurers now ask about COVID-19 in applications, and a positive test can mean a 30-to-60-day waiting period before a new policy is issued.

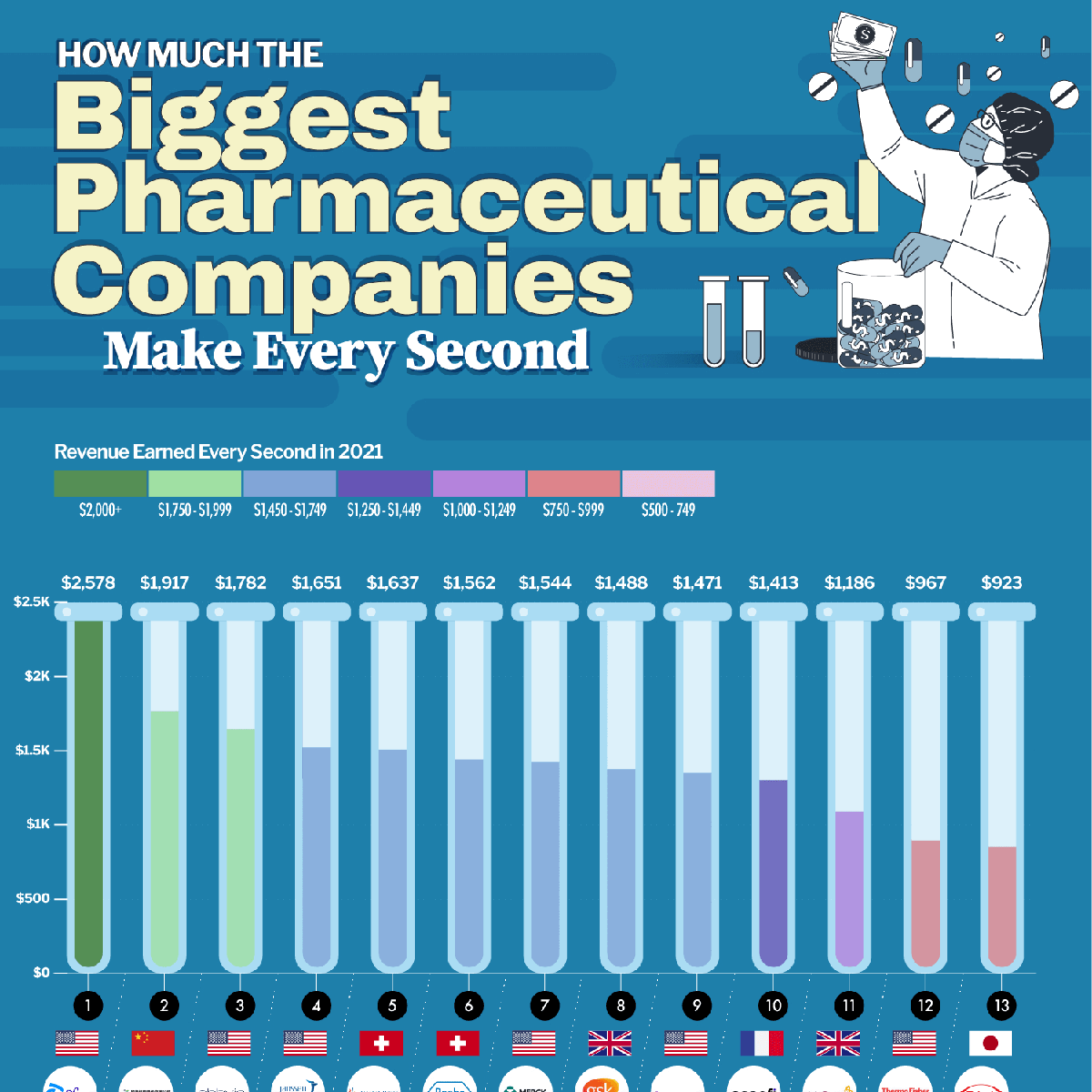

How Much the Biggest Pharma Companies Make Every Second

Insurancy broke down the annual revenue of the 25 biggest pharmaceutical companies into revenue per second. Pfizer topped the 2021 ranking at $2,578 earned every second, and the 2024 update shows Johnson & Johnson leading at roughly $2,816 per second based on full-year 2024 reports.

Insurtech Survey - Fitness Trackers and Life Insurance

Insurancy's insurtech survey of roughly 1,000 US respondents found 77% are uncomfortable with life insurance premiums that fluctuate based on yearly physicals, and 59% refuse to wear a fitness tracker that reports to insurers - even for a better rate. Younger respondents were the most resistant, complicating the industry's wearables push.

Investment Trends Study 2025 - Investor Statistics

Insurancy's investment trends study surveys how Americans invest: online apps, cryptocurrency, internet investing, robo-advisors, and the differences in how men and women approach the market.

Life Insurance Statistics 2026 - US Industry Facts

About 51% of American adults own life insurance according to LIMRA's 2025 Insurance Barometer Study, and ownership has drifted down from 63% in 2011. This report combines Insurancy's own consumer research with industry data on why people buy coverage, how they shop, and which companies write the most premiums.

Life Insurance Consumer Report 2025 - Key Findings

Insurancy's Life Insurance Consumer Report finds Gen X is the age group most likely to own life insurance and Gen Z the least likely, while marriage and children both raise ownership sharply. Notably, 70% of respondents now estimate the cost of life insurance correctly, challenging the long-held industry belief that consumers dramatically overestimate prices.

Online Shopping and E-commerce Statistics 2024 Study

Insurancy surveyed 2,400 US respondents about their online research and purchasing habits. The e-commerce study covers how shoppers use reviews and search, how mobile changes buying behavior, and what ultimately drives online purchases.

What Is Bereavement and End-of-Life Support?

Bereavement is the period of grief and mourning after the death of a loved one. Grief affects everyone differently, from anticipatory grief before a death to complicated grief that lingers. This guide explains the types and manifestations of grief and collects vetted resources for supporting the bereaved - and the end-of-life nurses who care for dying patients.

Life Insurance and COVID-19 Study - 2024 Findings

Insurancy's life insurance and COVID-19 study found 48.2% of respondents own a personal policy, interest in buying coverage rose slightly during the pandemic, and 3 in 4 people do not believe COVID-19 will be treated as a pre-existing condition. Concerns about rising rates were common, making early application the practical takeaway.

Car Insurance Without a License - How to Get Covered

You can get car insurance without a driver's license, usually by listing a licensed household member or caregiver as the primary driver and excluding yourself. Common reasons include owning a car someone else drives, keeping a stored or classic car covered, and protecting a vehicle for a teen or elderly relative.

Best Car Insurance for 16-Year-Olds - Rates and Discounts

The best car insurance for a 16-year-old is almost always to add them as a driver on a parent policy, which typically costs 40 to 60 percent less than a stand-alone policy for the same teen. Top insurers for teens include GEICO, State Farm, Progressive, and USAA (for military families), with good-student and driver-training discounts often stacking to 25 to 30 percent off.

Best Car Insurance for 17-Year-Olds - Cost and Discounts

The best car insurance for a 17-year-old is typically to stay on a parent policy as a listed driver, where the shared premium is roughly half the cost of a stand-alone teen policy. Nationally the cheapest carriers for 17-year-olds are USAA (military only), GEICO, State Farm, and Erie in the states where it operates. Good-student and defensive-driving discounts can cut 15 to 25 percent off the premium.

Best Car Insurance for 18-Year-Olds - Cost and Discounts

At 18, most drivers can legally sign their own auto policy, but the best car insurance for an 18-year-old is still typically to stay on a parent policy. A stand-alone policy for an 18-year-old averages about $3,600 to $5,200 a year, while adding an 18-year-old to a parent policy raises the family premium by roughly $1,800 to $2,400. Good-student and telematics discounts cut both by 15 to 25 percent.

Best Car Insurance for 19-Year-Olds - Rates and Savings

A 19-year-old typically pays roughly half what a 16-year-old pays for car insurance, but still 2 to 3 times what a 30-year-old pays. The best carriers for 19-year-olds nationally are GEICO, State Farm, Progressive, and USAA for military families. Good-student, student-away-at-school, and telematics (usage-based) discounts can cut the premium another 15 to 25 percent.

Best Car Insurance for 20-Year-Olds - Rates and Discounts

A 20-year-old typically pays $2,400 to $3,600 a year for a stand-alone auto policy, or about $1,200 to $1,800 in additional premium if added to a parent policy. Cheapest carriers nationally for 20-year-olds include GEICO, USAA, Erie, and State Farm. Good-student, defensive-driving, telematics, and multi-line (bundling with renters) discounts can stack to 20 to 30 percent off.

Best Car Insurance for 21-Year-Olds - Rates and Discounts

At 21, car insurance rates drop sharply as most carriers move drivers out of the youthful bracket. A 21-year-old typically pays $1,900 to $2,900 a year for a stand-alone policy. Cheapest carriers for 21-year-olds nationally are USAA (military only), GEICO, Erie, and State Farm. Good-student, defensive-driving, telematics, and renters or homeowners bundling discounts can cut premium another 20 to 25 percent.

Best Car Insurance for 22-Year-Olds - Rates and Discounts

A 22-year-old typically pays $1,700 to $2,700 a year for a stand-alone auto insurance policy, roughly 60 percent of what a 19-year-old pays and closing in on the national average. Cheapest carriers for 22-year-olds nationally are USAA (military only), GEICO, Erie, and State Farm. Continuous coverage, defensive-driving, telematics, and renters bundling discounts can cut premium another 20 percent.

Best Car Insurance With Bad Credit - Cheapest Companies

Drivers with bad credit pay significantly more for car insurance - poor credit can add roughly $1,500 a year versus excellent credit - but USAA, Farm Bureau, GEICO, and Nationwide consistently price it cheapest. Five states (California, Hawaii, Massachusetts, Michigan, and Washington) ban credit-based pricing entirely, and improving your score gradually lowers your premium.

Car Insurance in Mesa, AZ - Rates, Companies, Discounts

Mesa drivers pay close to the Arizona average of about $844 a year for car insurance and must carry the state's 25/50/15 minimum liability limits. As Arizona's third-largest city, with heavy East Valley commuter traffic on US 60 and Loops 101 and 202, Mesa rewards drivers who compare several quotes and stack good-driver, multi-policy, and vehicle-safety discounts.

Accelerated Death Benefit Rider - How It Works

An accelerated death benefit rider lets you withdraw part of your life insurance death benefit early if you are diagnosed as terminally ill, and often for critical or chronic illness too. Most modern policies include the rider at no extra cost, and the withdrawal is generally income-tax-free. It turns your life insurance into a source of funds while you are still living.

Can You Insure a Car You Don't Own? Non-Owner Coverage

You can often insure a car you don't own, though some states require the policyholder to match the name on the title. Where that is the case, a non-owner policy covers your liability while driving borrowed or rented cars, and adding yourself as a listed driver on the owner's policy is usually the simpler fix.

Car Insurance With a Suspended License - How to Get It

You can get car insurance with a suspended license, and you often must - many states require proof of coverage or an SR-22 filing before reinstating your license. The practical route is working with an independent agent who knows which carriers accept suspended-status drivers, and never driving until the suspension is lifted.

Benefits of Using an Independent Life Insurance Agency

An independent life insurance agency is licensed with many carriers rather than one, which lets it compare quotes and underwriting for the same applicant across dozens of insurers. Independent agents also stay with you across policy events like beneficiary changes, conversions, and claims, and they save time and money for buyers with complicated health, occupation, or coverage needs.

Dave Ramsey on Life Insurance - What He Recommends

Dave Ramsey recommends level term life insurance in the amount of 10 to 12 times your annual income for a term long enough to cover the years your family depends on you. He is famously against whole life and universal life. His advice is sound for most middle-class families but leaves gaps for buyers with estate, business, or long-horizon legacy goals.

21 Life Insurance Myths Debunked - What Is Actually True

Life insurance is one of the most misunderstood products in personal finance. This guide takes the 21 most common myths, from "term life is a waste of money" to "I am too young to need it," and answers each one with what the industry actually does. Most families are underinsured because of one of these myths.

Auto Insurance for a Rebuilt Title Car - What to Expect

You can get auto insurance on a car with a rebuilt title, but expect extra steps: most states require an official inspection, and many insurers offer only liability coverage on rebuilt titles. Average premiums run about $2,422 a year for full coverage and $1,244 for liability-only, a bit more than a comparable clean-title car.

Arizona Commercial Auto Insurance - Requirements and Rates

Arizona commercial auto insurance covers vehicles used for business purposes and carries the same 25/50/15 minimum liability limits as personal policies, though most businesses need considerably higher limits. Any car, truck, van, or SUV used for business counts as a commercial vehicle, and personal policies typically exclude business-use claims.

Disability Income Rider on Life Insurance - How It Works

A disability income rider adds a monthly cash benefit to your life insurance if you become totally disabled and cannot work. It is usually a fixed dollar amount (often 1 percent of the face amount per month) paid for a set period after an elimination period. It is a cheap add-on for basic income protection but is not a substitute for a full disability insurance policy.

6-Month vs 12-Month Auto Insurance - Which Is Cheaper?

A 6-month auto insurance policy costs about the same per month as a 12-month policy - the real difference is flexibility versus rate lock. A 6-month term lets you re-shop or switch carriers twice a year, while a 12-month term locks your rate for a full year, which helps if you get a ticket or file a claim mid-policy. Full-coverage 12-month premiums for a typical driver run about $1,400 to $2,580.

Is Life Insurance Worth It? When It Is and When It Is Not

Life insurance is worth it when someone depends on your income or the work you do, including a spouse, kids, a business partner, or an aging parent. Term life is inexpensive during the years of highest need, permanent life fits a smaller set of estate, business, and legacy goals, and going without coverage leaves your family exposed to the lump-sum shock of a lost income.

Is Primerica a Pyramid Scheme? What to Know Before Buying

Primerica is a publicly traded life insurance company (NYSE: PRI) that sells through a multi-level marketing (MLM) sales force. It is not a pyramid scheme in the legal sense because it sells a real product, but its MLM structure means most recruits never earn meaningful income and its term life prices tend to run above independent-agent quotes for the same face amount. Comparing quotes elsewhere is smart before signing up.

Life Flight Insurance - Air Ambulance Membership Explained

Life Flight and other air-ambulance memberships cover the balance-billing gap that health insurance often leaves behind after an emergency medical flight. A single air-ambulance trip can bill $40,000 or more, and membership plans keep the out-of-pocket cost predictable for a small annual fee. It is a niche protection worth considering if you live in a rural area or travel remote regions.

Mortgage Life Insurance - Do You Need It? Alternatives

Mortgage life insurance is designed to pay off your home loan if you die during the mortgage term. The benefit shrinks with your loan balance and the lender is typically the beneficiary. A standard level term policy usually costs less, covers more, and lets your family choose how to spend the payout, which is why most buyers pick term over mortgage life.

Mutual of Omaha Cancer, Heart Attack, and Stroke Insurance

Mutual of Omaha sells a supplemental critical illness policy that pays a lump-sum cash benefit if you are diagnosed with cancer, a heart attack, or a stroke. The benefit is paid directly to you and can cover deductibles, income gaps, or non-medical expenses. It is designed to fill the cost gaps that major medical insurance leaves after a serious diagnosis.

Washington State Long-Term Care Tax (WA Cares) Explained

Washington State charges a 0.58 percent payroll tax through the WA Cares Fund to pay for a $36,500 lifetime long-term care benefit for eligible workers. Workers who owned private long-term care coverage before November 1, 2021 could apply for a permanent opt-out, and specific groups such as veterans with disabilities and out-of-state workers can also be exempt. Understanding the rules helps Washington residents plan their care.

Simplified Issue Whole Life Insurance - No Exam, Lifelong

Simplified issue whole life insurance skips the medical exam and asks a short set of health questions instead, then locks in a fixed premium and a lifelong death benefit with cash value. It fits buyers who want permanent coverage without waiting weeks for underwriting, though prices run higher than fully underwritten policies for the same face amount.

Long-Term Care Rider on Life Insurance - How It Works

A long-term care rider on a life insurance policy lets you use part of your death benefit to pay for qualified long-term care costs like a nursing home, home health aide, or assisted living. It builds LTC coverage into a policy you would already own, and unlike stand-alone LTC insurance, the death benefit still pays out to your family if you never need care.

Adjustable Life Insurance - How It Works and Who It Fits

Adjustable life insurance is a form of permanent coverage where you can change the death benefit, premium payments, and cash-value schedule as your finances shift. It offers more flexibility than whole life and can adapt to new dependents, higher income, or a paid-off mortgage, in exchange for closer attention to funding and periodic reviews.

Best Car Insurance for a Bad Driving Record - Your Options

Most insurers will still cover drivers with accidents, tickets, or a DUI - the trade-off is a higher premium for the 3 to 5 years insurers look back on your record. The best policy for a bad driver is the least expensive one that still carries adequate protection, and rates improve at each renewal as violations age off.

Brian Greenberg - Million Dollar Round Table Member

Insurancy founder and CEO Brian Greenberg has been a member of the Million Dollar Round Table (MDRT) since 2013. MDRT is the premier global association for life insurance and financial services professionals, and membership is limited to about the top 1 percent of advisors worldwide.

Indexed Universal Life Insurance Guide - IUL Explained

Indexed universal life insurance is a permanent policy that credits cash-value growth based on the performance of a stock index like the S&P 500, subject to a floor and a cap. IUL gives more upside than whole life without direct market losses, plus flexible premiums, but caps, participation rates, and policy charges make it a long-horizon product, not a market fund.

Personal Loan Protection Insurance - Is It Worth It?

Personal loan protection insurance is a policy sold with a personal loan that pays some or all of the balance if you die, become disabled, or in some cases lose your job. It is convenient, but a standard level term life policy paired with disability insurance usually delivers more coverage per dollar and follows you across every debt, not just this one loan.

Rental Car Insurance - Do You Need It and What It Covers

Rental car insurance covers liability and damage while you drive a rental, but you may not need to buy it at the counter - your personal auto policy often extends to rentals, and many credit cards include complimentary rental coverage. Check both before paying for duplicate protection.

Why Compare Auto Insurance Quotes Online Before You Buy

Comparing auto insurance quotes online is the fastest way to see how much rates vary between companies for the exact same driver - often by hundreds of dollars a year. Online quotes are free, generally accurate if you enter honest information, and comparison tools can pull multiple company rates at once.

What to Do When You Get in a Car Accident - 8 Steps

After a car accident, check for injuries first, call the police even for minor crashes, exchange information, photograph the scene, seek medical attention, and notify your insurance company promptly. NHTSA counted 42,514 traffic fatalities in 2022, and a calm, documented response protects both your health and your claim.

Pulled Over While High on Marijuana? What to Do Next

If you get pulled over while high on marijuana, stay calm, keep your answers short, and do not consent to a vehicle search. Every state can charge drugged driving as a DUI - including states where marijuana is legal - and some use zero-tolerance or per se THC limits. If you are arrested or charged, contact a defense attorney experienced with marijuana DUI cases right away.

Pulled Over for DUI? 7 Steps to Protect Yourself

If you get pulled over for DUI, stay calm, pull over safely, be polite, and say as little as possible. Field sobriety tests and hand-held breathalyzers are voluntary in most states, but refusing the chemical test at the station after an arrest triggers implied-consent penalties like automatic license suspension. Call an experienced DUI attorney as soon as possible after any arrest.

Best Insurance for a Leased Car - Coverage and Gap Rules

The best insurance for a leased car is the lowest-premium policy that satisfies both your state minimums and your leasing company's requirements - typically full coverage, often with gap insurance on top. Leasing itself does not raise the premium; identical coverage costs the same whether the car is leased or owned.

Best Car Insurance for Commuters - Mileage and Rates

The best car insurance for commuters is the cheapest policy that still protects you at commuter mileage, because insurers charge more once annual miles climb past pleasure-use caps of roughly 8,000 to 15,000. Every major carrier writes commuter policies, so comparing quotes at your true mileage is what separates a fair rate from an inflated one.

What Is an Auto Insurance Binder? Proof Before Your Policy

An auto insurance binder is a temporary document that proves you have coverage while your formal policy paperwork is being finalized. It lists the driver, insurer, coverages, premiums, VIN, and policy number, costs nothing beyond the policy itself, and is most often needed when financing a car, at the DMV, or after switching insurers.

Comprehensive Auto Insurance - Coverage, Cost, Deductibles

Comprehensive auto insurance pays to repair or replace your car when it is damaged by something other than a collision - theft, weather, fire, falling objects, vandalism, or animal strikes. It averages about $194 a year with a typical $500 deductible, and lenders and leasing companies require it even though state law does not.

Collision Auto Insurance - What It Covers and Costs

Collision insurance pays to repair or replace your own car after an accident, regardless of who was at fault. It is optional under state law but required by most lenders and leasing companies, and the average cost inside a full-coverage policy ran roughly $1,080 to $1,350 a year as of 2020. Your deductible decides how much you pay out of pocket before coverage kicks in.

Cheap Car Insurance in Arizona - Rates by City and Tips

Cheap car insurance in Arizona starts with the state minimum of $25,000 bodily injury per person, $50,000 per accident, and $15,000 property damage - and rates vary noticeably between Phoenix, Tucson, Mesa, Scottsdale, and other cities. Your driving record, credit, vehicle, and ZIP code shape the premium, so comparing quotes city by city is the core money-saver.

Georgia Commercial Auto Insurance - Requirements and Costs

Georgia commercial auto insurance is required for vehicles used for business purposes, with minimum limits of $25,000 bodily injury per person, $50,000 per accident, and $25,000 property damage. It works like personal auto insurance but is built for business risks, higher limits, and employee drivers.

Do Car Dealerships Offer Temporary Insurance? What to Know

Most major car dealerships can arrange temporary insurance for a new purchase, but you still need proof of coverage before financing or leasing a vehicle off the lot. Existing policies often cover a new car for a 2-to-30-day grace period depending on the state and insurer, and a 30-day temporary term is usually the practical choice while you shop for a long-term policy.

Car Insurance in Tucson, AZ - Rates, Minimums, Companies

Tucson drivers must carry Arizona's minimum liability limits of $25,000 bodily injury per person, $50,000 per accident, and $15,000 property damage. As Arizona's second-largest city, with I-10 and I-19 running through it, Tucson generally sees rates below the Phoenix metro - and shopping several quotes is still the surest way to find a cheap policy.

Car Insurance in Scottsdale, AZ - Rates and Top Companies

Full coverage car insurance in Scottsdale averages about $1,673 a year, slightly above the Arizona state average of $1,574 - pricier vehicles and busy Loop 101 commuter traffic both play a part. Scottsdale drivers can close the gap by comparing top-rated insurers and choosing coverage deliberately rather than defaulting to the cheapest quote.

Married vs Single Car Insurance Rates - Why Singles Pay More

Single drivers typically pay more for car insurance than married drivers with identical driving records, because insurers associate marriage with statistically fewer claims. There is no specific married discount - marital status is simply one of many rating factors - and single drivers can close most of the gap by comparing quotes and stacking other discounts.

Do You Need Insurance to Register a Car? State Rules

Most states require proof of insurance before you can register a car, and at minimum you will need your state's required liability coverage. A handful of states let you register before buying coverage or check insurance electronically later, but driving uninsured is illegal in every state except New Hampshire.

Does Auto Insurance Follow the Car or the Driver?

Auto insurance generally follows the car, not the driver - if someone borrows your car with permission and crashes, your policy typically pays first. Certain supplemental coverages, like rental car protection and some liability extensions, follow the driver instead. Who pays after an accident depends on fault, policy exclusions, and whether the driver was permitted.

Food Truck Insurance - Coverage, Cost, and 5 Top Companies

Food truck insurance bundles commercial auto, general liability, and property protection for your mobile kitchen. Progressive, Nationwide, GEICO, State Farm, and The Hartford all write competitive food truck policies, and costs vary with the truck's value, your location, menu, and coverage level.

Hired and Non-Owned Auto Coverage (HNOA) - What It Covers

Hired and non-owned auto coverage (HNOA) protects your business from liability when employees or contractors drive rented, hired, or personal vehicles for work. It fills the gap left by commercial auto insurance, which only covers vehicles the business owns, and it is essential once employees run errands, deliver, or travel in cars the company does not own.

Car Insurance When Moving to a New State - What to Update

Moving to a new state usually means updating or replacing your car insurance policy, and most states give you 30 to 90 days after the move to do it. Start with a call to your current agent before you move, expect your rate to change with your new ZIP code, and be ready to switch carriers if your insurer is not licensed in the new state.

What Is Supplemental Life Insurance? How It Works

Supplemental life insurance is extra coverage added on top of a basic policy, most often through your employer. Basic group plans cover a fixed amount or salary multiple, and supplemental coverage raises that limit for an extra premium. It is convenient, but not always portable, which is why many people pair it with an individual policy they own.

Jobs and Hobbies That Raise Life Insurance Rates

Dangerous work and hobbies raise life insurance prices because they raise the odds of an early claim. Insurers flag occupations like logging, roofing, and aviation, and hobbies like skydiving and scuba diving, then add a flat extra charge or assign a higher rate class. Honest disclosure and the right carrier match keep coverage affordable.

Why Women Need Life Insurance - Key Stats and Reasons

Women are underinsured compared to men despite earning, caregiving, and living longer. A stay-at-home mom's labor would cost a full-time salary to replace, women make up nearly half the workforce, and family history factors like BRCA affect insurability, which makes locking in coverage early especially valuable for women.

Group Life Insurance Through Associations - A Guide

You do not need an employer to get group life insurance: professional, fraternal, and membership associations offer group term and whole life plans to members with simplified underwriting and group pricing. It is a practical route for people without workplace coverage, though group coverage alone is rarely enough for a family's full needs.

Marijuana and Life Insurance - How Insurers Rate THC

Marijuana users can absolutely buy life insurance. Rates depend mostly on frequency of use: occasional users can land standard or better classes at marijuana-friendly carriers, while frequent users are often rated in the smoker class. Insurers verify use through THC testing, application answers, and MIB records, so honesty is essential.

Life Insurance for Young Adults - Why Buying Early Wins

Life insurance is cheapest when you are young and healthy, and the rate you lock in lasts the whole term. Term life delivers the most coverage per dollar for young families, whole life starts building cash value early, and no medical exam policies make applying fast. Waiting only raises the price of the same coverage.

Life Insurance for Seniors - Best Options by Age

Retiring does not end your life insurance options. Healthy seniors can still buy level term policies, final expense policies cover funeral costs with simplified underwriting, and guaranteed acceptance policies skip health questions entirely in exchange for graded benefits. The right choice depends on your age, health, and what you need the payout to do.

Life Insurance for Married Couples - Joint or Separate?

Life insurance is a smart move for most married couples, and the first decision is joint versus separate policies. Separate policies pay a benefit at each death and can be sized to each spouse's income, while joint first-to-die or survivorship policies cover two people under one contract but pay only once. Domestic partners can qualify too.

Life Insurance While Pregnant - How to Get Approved

Pregnancy does not disqualify you from life insurance. Insurers review your pre-pregnancy health and weight along with any complications, and the first trimester is generally the easiest window to get approved at your normal rate class. A growing family is exactly when coverage matters most.

Business Overhead Expense (BOE) Insurance - How It Works

Business overhead expense (BOE) insurance reimburses your business's fixed costs, rent, payroll, utilities, insurance, and loan payments, if a disability keeps you from working. It keeps the lights on so the business survives your recovery. BOE complements, not replaces, individual disability income insurance: BOE pays the business's bills while disability income replaces your personal paycheck.

Life Insurance Underwriting Process - Step by Step

Underwriting is how a life insurer turns your application into a price: an underwriter reviews your health history, exam results, prescription records, MIB report, driving record, and lifestyle to assign a rate class. The process runs from instant (accelerated) to several weeks (fully underwritten), and preparation, honest answers, and the right carrier match improve the outcome.

Workers Comp Insurance for Small Business - What to Know

Most states require workers compensation as soon as a small business hires its first employee, and even where thresholds are higher, going without coverage exposes the business to lawsuits and fines. Coverage pays employee medical costs and lost wages after work injuries. Premiums scale with payroll and industry risk, which keeps costs manageable for most small teams.

Workers Compensation Insurance Guide - Costs and Coverage

Workers compensation insurance pays medical bills, lost wages, and rehabilitation costs when an employee is injured or made ill by their job, and it protects the employer from most injury lawsuits in return. Nearly every state requires coverage once you hire employees, benefit formulas vary by state, and premiums are driven by payroll, class codes, and your claims history.

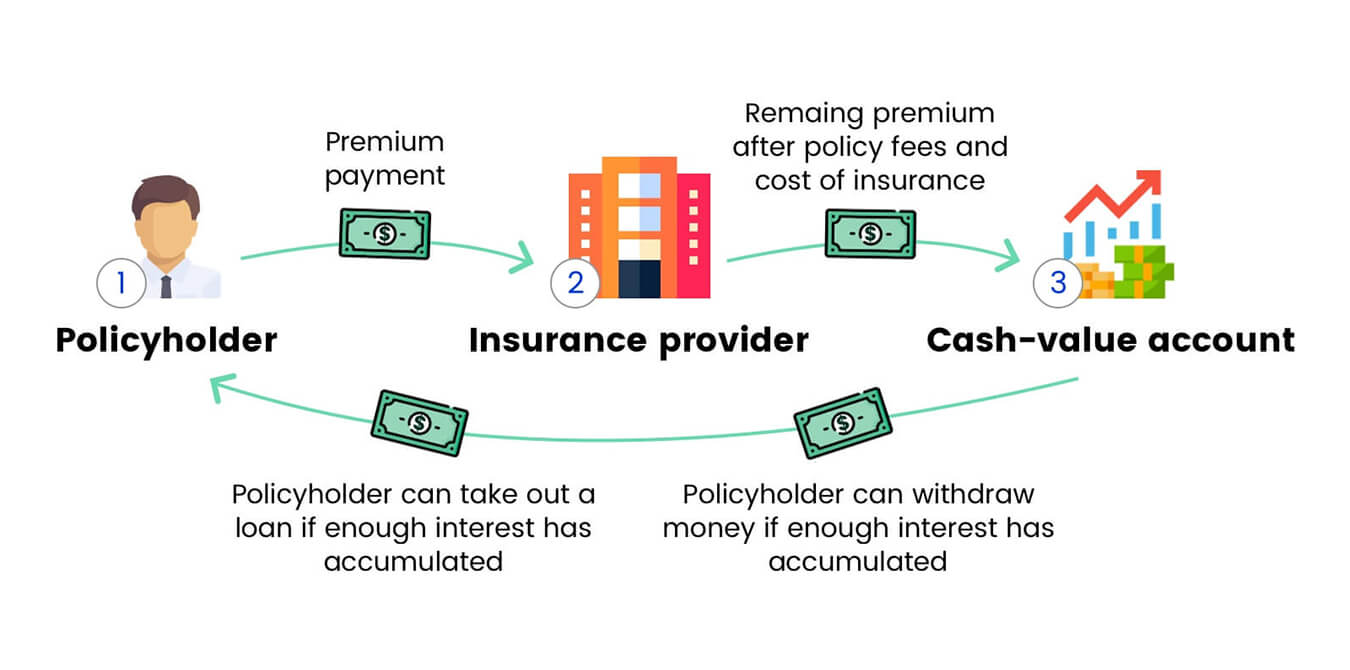

Single Premium Life Insurance - Pay Once, Covered for Life

Single premium life insurance (SPL) is permanent coverage purchased with one lump-sum payment instead of ongoing premiums. The policy is guaranteed paid-up from day one and builds cash value immediately, which makes it a wealth transfer tool for people with idle savings. The tradeoff is tax treatment: nearly every SPL policy is a modified endowment contract (MEC), so lifetime withdrawals and loans are taxed earnings-first with a penalty before age 59 and a half.

Graded Benefits vs Contestability - Key Differences

Graded death benefits and the contestability period both affect early claims but are different mechanisms. Graded benefits are a product feature of guaranteed issue policies: natural-cause payouts phase in over two to three years. Contestability is a legal window, typically the first two years of any policy, when the insurer can investigate claims and rescind coverage for material misrepresentation on the application.

Workers Comp for Self-Employed Contractors - Do You Need It

Most states do not require self-employed contractors with no employees to carry workers compensation, but the market often does: general contractors, commercial clients, and some licensing boards demand proof of coverage before you can work. Options include buying a policy that covers you personally or, where accepted, a certificate of exemption.

Life Insurance Waiting Periods - Graded Benefits Explained

Most fully underwritten life insurance has no waiting period: coverage is effective the day the policy is in force. Waiting periods belong to guaranteed issue and some simplified issue final expense policies, which phase in the death benefit over the first two to three years, typically refunding premiums plus interest if death occurs from natural causes during the graded window. Accidental deaths are usually covered in full from day one.

Irrevocable Life Insurance Trust (ILIT) - How It Works

An irrevocable life insurance trust (ILIT) is a non-amendable legal structure that owns a life insurance policy so the death benefit stays outside the insured's taxable estate. The grantor funds premiums with annual exclusion gifts, beneficiaries receive Crummey withdrawal notices that qualify those gifts for the $19,000 annual exclusion, and at death the trustee collects and distributes the benefit under the trust terms.

What Is LexisNexis? How Insurers Use Your Data

LexisNexis Risk Solutions is a data broker life insurers rely on during underwriting: it supplies motor vehicle records, prescription histories, public records, and its Risk Classifier score that predicts mortality risk from data instead of labs. It powers many instant-decision products. You have the right to request your LexisNexis consumer file and dispute errors under the FCRA.

When Do You Need Business Insurance? Key Trigger Points

The right time to buy business insurance is before the risk exists, and specific events make it non-negotiable: signing a commercial lease, hiring your first employee, taking on client contracts that require proof of coverage, buying business property, or opening to the public. Waiting until after a loss means the loss is not covered.

Commercial Umbrella Insurance - Extra Liability Coverage

Commercial umbrella insurance sits on top of your existing liability policies, general liability, commercial auto, and employer's liability, and pays when a covered claim exceeds their limits. A single serious accident or lawsuit can blow past a standard $1 million limit, and umbrella coverage delivers extra millions of protection at a comparatively low premium.

Professional Liability Insurance (E&O) - What It Covers

Professional liability insurance, also called errors and omissions (E&O) coverage, protects service providers when a client claims your work was negligent, wrong, or incomplete and cost them money. It covers legal defense and settlements for professional mistakes, the exact claims general liability excludes, and it is standard for consultants, agents, accountants, designers, and anyone paid for advice or expertise.

How No Exam Life Insurance Works - Instant Underwriting

No exam life insurance replaces the needle and the nurse with data: insurers verify prescription histories, MIB records, motor vehicle reports, and application answers, then run them through underwriting models that can approve qualifying applicants in minutes. Healthy applicants get real fully underwritten pricing without labs, while guaranteed issue products serve those who cannot qualify.

How Long Does a Life Insurance Application Take? Timeline

The life insurance application timeline depends on the underwriting path. No-exam accelerated underwriting can approve qualifying applicants the same day. Fully underwritten policies typically take four to eight weeks: application, exam scheduling, lab results, medical records requests, underwriting review, and offer. Records requests from doctors' offices are the most common bottleneck.

Is Workers Comp Taxable? IRS Rules for Benefits and Wages

Workers compensation benefits are generally not taxable at the federal or state level: IRS Publication 525 excludes amounts received under workers compensation acts for occupational injury or sickness. The main exception arises when benefits offset Social Security disability payments, making a portion effectively taxable. For employers, premiums are a deductible business expense.

Hazard Insurance for Business - What It Is and Who Needs It

Hazard insurance for business is another name for the commercial property coverage that protects your buildings and equipment against fire, storms, vandalism, and other named perils. The term shows up most often in lending: SBA and conventional lenders require proof of hazard insurance on business assets pledged as collateral before funding a loan.

Living Will vs Living Trust - What Each Does and Costs

A living will and a living trust solve two different problems. A living will is an advance directive that records your medical treatment wishes if you cannot speak for yourself. A living trust is a legal entity that holds your assets during life and passes them to beneficiaries without probate. Most complete estate plans include both, alongside a last will and durable powers of attorney.

Do LLCs Need Business Insurance? Why the Shield Falls Short

Forming an LLC protects your personal assets from business debts, but it does nothing to protect the business itself. A lawsuit, fire, or injured employee can still wipe out everything the LLC owns. That is why LLCs still carry general liability, commercial property, and workers compensation coverage, and why courts can pierce the veil of an underinsured LLC.

Does Business Insurance Cover Theft? Property vs Crime

Business insurance does cover theft, but which policy pays depends on who stole what. Commercial property insurance covers theft of equipment and inventory by outsiders, usually with signs of forced entry. Employee theft, embezzlement, and stolen cash need commercial crime (fidelity) coverage, and stolen customer data falls to cyber insurance.

General Liability Insurance for Small Business - Coverage

General liability (GL) insurance is the foundation policy for small businesses: it pays for third-party bodily injury, damage to other people's property, and personal or advertising injury claims, including the legal defense costs that come with them. It does not cover your own property, your employees' injuries, or professional mistakes, which need property, workers comp, and E&O policies respectively.

Does Personal Auto Insurance Cover Business Use? The Rules

Personal auto insurance generally does not cover business use of a vehicle: policies exclude commercial activity, and a claim that happens while working can be denied outright. Commuting is fine; deliveries, hauling tools to job sites, transporting clients, and rideshare work are not. Regular business use calls for a commercial auto policy or, for occasional use, specific endorsements.

How Is Workers Comp Calculated? Premiums and Benefits

Workers compensation math runs on two formulas. Premiums are calculated from payroll (per $100), industry class codes, and an experience modifier reflecting your claims history. Benefits paid to injured workers are a state-set percentage of their average weekly wage, commonly about two-thirds, subject to state maximums and time limits.

How Much Is Commercial Auto Insurance? Cost Factors

Commercial auto insurance pricing is driven by what you drive, who drives it, and what you haul: vehicle type and value, driver records, coverage limits, radius of operation, and industry all move the number. Businesses with clean drivers and light vehicles pay far less than those running heavy trucks, and higher liability limits required by contracts raise premiums.

How Much Is Commercial Trucking Insurance? Cost Breakdown

Commercial trucking insurance is one of the largest operating costs in the industry. Premiums are driven by what you haul, how far you run, driver experience and records, equipment value, and the federal liability minimums that apply to your operation. Owner-operators with their own authority pay the most; leased drivers under a motor carrier's program pay far less.

Business Personal Property Insurance - What BPP Covers

Business personal property (BPP) insurance covers the contents of your business: equipment, inventory, furniture, fixtures, tools, and supplies, against fire, theft, vandalism, and other covered perils. It is the "stuff" half of commercial property coverage, distinct from the building itself, and it is typically bundled inside a business owners policy (BOP).

What Insurance Is Needed for a Small Business? Full Guide

Most small businesses need three coverages at minimum: general liability for third-party injury and property damage claims, commercial property for the business's own assets, and workers compensation once employees are hired. Industry, contracts, lenders, and state law then layer on requirements like commercial auto, professional liability, and cyber coverage.

Restaurant Insurance Programs - Coverage and Ways to Save

Restaurant insurance programs bundle the coverages food businesses need most: general liability, commercial property, workers compensation, liquor liability, spoilage, and business interruption, often at package pricing below buying each policy separately. Premiums track your square footage, payroll, alcohol sales, and claims history, and several practical steps cut costs without thinning protection.

Is Business Insurance Tax Deductible? IRS Rules Explained

Business insurance premiums are generally tax deductible because the IRS treats them as ordinary and necessary business expenses. General liability, commercial property, workers comp, commercial auto, professional liability, and cyber premiums all typically qualify. The notable exceptions: life insurance where the business is the beneficiary, and certain self-insurance reserves. Confirm specifics with your tax professional.

Employers Liability vs Workers Comp - What's the Difference

They travel together but do different jobs. Workers compensation (Part One of the policy) pays injured employees' medical bills and lost wages regardless of fault. Employer's liability insurance (Part Two) defends the business when an employee sues anyway, alleging negligence outside the no-fault system, covering legal defense, settlements, and judgments.

Does Life Insurance Cover Suicide? The 2 Year Clause

Most life insurance policies cover suicide once the suicide clause expires, typically two years after the policy is issued. If death occurs inside that exclusion window, the insurer usually refunds the premiums paid instead of paying the death benefit. Group life policies often carry no suicide clause at all, and replacing a policy restarts the clock.

Private Placement Life Insurance (PPLI) - How It Works

Private placement life insurance (PPLI) is a variable universal life policy offered privately to accredited investors and qualified purchasers. Inside the policy, premiums flow into insurance-dedicated funds spanning hedge fund and institutional strategies, growing tax deferred with an income tax free death benefit. PPLI demands large commitments, strict diversification, and hands-off investor behavior, which limits it to high net worth planning.

Million Dollar Life Insurance - Cost and How to Qualify

A million dollar life insurance policy is standard planning, not a luxury, for households replacing a solid income: coverage of 10 to 15 times annual income puts many families squarely at seven figures. Healthy applicants find level term at this size surprisingly affordable, insurers verify income to justify the amount, and accelerated underwriting now approves qualifying buyers for $1 million or more with no medical exam.

MIB Report - What Life Insurers Know About You

MIB (formerly the Medical Information Bureau) is a member-owned data exchange life insurers use to cross-check applications. Your MIB report contains coded flags from previous individual life, health, and disability applications: reported conditions, lab abnormalities, and hazardous activities. You can request your file free once a year directly from MIB and dispute anything inaccurate.

Life Insurance to Secure an SBA Loan - What Lenders Require

SBA lenders routinely require life insurance before closing when a business depends on its owner: a policy at least equal to the loan amount, with a collateral assignment giving the lender first claim until the debt is repaid. Term life fits best, and no-exam accelerated underwriting means even a tight closing timeline is workable for healthy applicants.

Life Insurance Policy Features and Types Explained

Policy features decide who a policy fits. Accidental policies pay only for accidents, graded and modified benefit policies phase in payouts for higher-risk buyers, no exam and rapid issue policies trade labs for speed, guaranteed issue asks no health questions, return of premium refunds your payments if you outlive the term, and living benefits let you use the policy while alive.

Collateral Assignment of Life Insurance - How It Works

A collateral assignment of life insurance gives a lender a priority claim on your policy's death benefit until a loan is repaid. SBA lenders routinely require it when a business depends on the owner. The lender is repaid first from the death benefit if you die with a balance outstanding, your beneficiaries receive the remainder, and the assignment is released once the loan is satisfied.

Life Insurance for Estate Planning - Taxes and Trusts

Life insurance is one of the most flexible tools in estate planning: the death benefit passes to named beneficiaries income tax free and outside probate, and it can pay estate taxes and settlement costs, equalize inheritances, and fund trusts. With the federal estate tax exemption at $15 million per person for 2026, most estates owe no federal tax, but state estate taxes and liquidity needs keep coverage central to many plans.

Life Insurance Dividends - How They Work and Your Options

Life insurance dividends are a share of a mutual insurer's favorable results paid to participating whole life policyholders. Dividends are not guaranteed, but carriers like MassMutual, Penn Mutual, Guardian, and Foresters have long track records of paying them. Policyholders choose among five uses: take cash, reduce premiums, leave them to accumulate at interest, repay policy loans, or buy paid-up additions that compound coverage and cash value.

Life Insurance Definitions - Glossary of Key Terms

Life insurance has a vocabulary all its own. This glossary defines the terms buyers meet most often: the death benefit your beneficiaries receive, the premium you pay, cash value inside permanent policies, riders that add features like accelerated death benefits, and the underwriting classes that set your price.

Imputed Income and Life Insurance - The $50,000 GTL Rule

Imputed income is the taxable value of employer-paid group term life insurance above $50,000 of coverage. The IRS sets the value using its Table I uniform premium rates based on your age, and the amount appears on your W-2 (Box 12, Code C) and is subject to Social Security and Medicare taxes. The first $50,000 of employer-paid coverage stays tax free.

How to Find Out if Someone Has Life Insurance - 6 Steps

Start with the free NAIC Life Insurance Policy Locator, which asks participating insurers to search for policies in the deceased's name. From there, check personal papers and bank statements for premium payments, ask employers about group coverage, search state unclaimed property databases, and consider an MIB policy search for applications made after 1996.

Life Insurance Rate Classes - How Insurers Decide Yours

Your rate class is the single biggest driver of your life insurance price. Insurers sort applicants into classes like Preferred Plus, Preferred, Standard Plus, and Standard (plus table ratings below that) based on health history, build, blood work, family history, driving record, and nicotine use. Each carrier draws the lines differently, which is why shopping the same profile across carriers changes the quote.

Funding a Buy-Sell Agreement with Life Insurance - Guide

A buy-sell agreement is a contract that fixes what happens to an owner's share of the business at death, and life insurance is the standard way to fund it: the policy delivers the exact cash needed to buy out the deceased owner's stake the moment it is needed. The two classic structures are cross-purchase, where owners insure each other, and entity purchase, where the business owns the policies.

Does Life Insurance Cover Funeral Costs? How It Works

Beneficiaries can absolutely use a life insurance payout for funeral costs, though nothing requires them to: the death benefit arrives as a lump sum spent at their discretion. If covering final costs is the whole goal, a small final expense (burial) policy is built for exactly that, with simplified underwriting and face amounts sized to funeral bills.

How to Use Life Insurance While Alive - Living Benefits

Several kinds of life insurance pay benefits while you are alive. Permanent policies build cash value you can borrow against, withdraw, or surrender, and many policies offer living benefit riders that accelerate the death benefit after a serious diagnosis. The tradeoff: money used while living typically reduces what your beneficiaries receive.

How to Cancel a Life Insurance Policy - Rules and Costs

You can cancel a life insurance policy at any time by stopping payments or writing to the insurer. Term cancellations return little or nothing outside the free look window, while permanent policies pay the cash surrender value minus any surrender charge. Before canceling, compare alternatives like reducing coverage, using cash value to pay premiums, or selling the policy in a life settlement.

Can You Retake a Life Insurance Medical Exam? Your Options

If your life insurance exam results came back worse than expected, you usually can retake the exam or ask the insurer to re-run specific labs, though carriers differ on timing and rules. Often the smarter play is applying to a different carrier whose underwriting treats your specific issue more favorably, or waiting a few months to correct a temporary result before re-testing.

How Many Life Insurance Policies Can You Have?

You can own as many life insurance policies as you like, from one insurer or several. The practical cap is total coverage: underwriters justify your combined death benefit against income and financial obligations. Laddering multiple term policies is the most popular reason to hold several, letting coverage and premiums step down as debts get paid off.

Are Life Insurance Premiums a Deductible Business Expense?

Life insurance premiums are generally not a deductible business expense when the business is a direct or indirect beneficiary, which covers key person coverage and policies backing buy-sell agreements. The main exception is employer-paid group term life for employees: premiums are deductible, and the first $50,000 of coverage per employee is also excluded from the employee's income.

9 Ways Life Insurance Will Not Pay Out - Denied Claims

Life insurance almost always pays, but nine situations can void a payout: death during the two year suicide exclusion, withholding information on the application, dangerous activities, illegal activities, act of war clauses, living outside the United States, fraud, missing insurable interest, and lapses caused by policy replacement. Honest applications and premiums paid on time prevent nearly all of them.

DUI and Life Insurance - How Rates and Approval Change

A DUI makes life insurance more expensive but rarely uncoverable. Carriers care most about how recent the offense is: within the first year or two, many decline or offer table ratings; after three to five clean years, several carriers return to standard classes; and older single offenses can even reach preferred at the most forgiving insurers. Carrier selection matters more here than almost anywhere.

Court-Ordered Life Insurance in Divorce - How It Works

Courts routinely order a divorcing spouse to carry life insurance so alimony and child support survive their death. The paying spouse typically owns the policy with the ex-spouse as beneficiary, sized to the support obligation and its duration. Instant-decision term policies can put coverage in force the same day, which matters when a decree sets a deadline.

AIG Life Insurance Review - Now Corebridge Financial

AIG no longer sells life insurance under the AIG brand: its life and retirement division became Corebridge Financial, which went public in 2022 and completed its separation from AIG. Policies continue to be issued by American General Life Insurance Company, rated A (Excellent) by A.M. Best. Existing AIG life policies remain fully in force, and the product shelf, led by Select-A-Term with its 18 term-length choices and the QoL living benefit riders, continues under the Corebridge name.

Americo Life Insurance Review - Mortgage Protection Focus

Americo Financial Life and Annuity, headquartered in Kansas City with corporate roots tracing to 1906, is one of the biggest names in agent-sold mortgage protection term life. Its shelf also includes final expense whole life (the Eagle series) and universal life, all built around simplified, no-exam underwriting and independent agent distribution. Americo fits homeowners approached about mortgage protection and final expense buyers, though comparing against level term always belongs in the process.

Great Western Life Insurance Review - Exited the Market

Great Western Insurance Company, a Utah-based final expense specialist, no longer sells new life insurance policies. Existing policies remain in force and continue to be serviced. Final expense shoppers today should compare active specialists such as Mutual of Omaha and Aetna's Accendo brand, which offer similar simplified-issue burial coverage.

Primerica Life Insurance Review

Primerica is an A+ rated (Superior) life insurer founded in 1977 and headquartered in Duluth, Georgia. It sells term life insurance exclusively, no whole life or universal life, through a network of more than 140,000 licensed representatives, built around the Buy Term and Invest the Difference philosophy. Coverage is solid and the company is financially strong, but policies are only available through a Primerica rep and pricing is often higher than broker-sold term.

SureBridge Insurance Review - Supplemental Health Plans

SureBridge is a supplemental insurance brand, not a life insurance company: its accident, critical illness, hospital, dental, and vision products are underwritten by The Chesapeake Life Insurance Company, part of the UnitedHealthcare family. Supplemental policies pay cash benefits for covered health events, which complements but does not replace life insurance. Shoppers who landed here looking for death benefit protection should compare term life carriers.

United Home Life Review - Express Issue No-Exam Policies

United Home Life Insurance Company, an Indianapolis-based insurer affiliated with United Farm Family Life, specializes in Express Issue simplified products: no-exam term and whole life with tiered acceptance that reaches tougher health histories, including options marketed to applicants declined elsewhere. Face amounts are modest and per-dollar pricing reflects the easy underwriting, making it a niche tool rather than a primary family-coverage carrier.

Lincoln Financial Life Insurance Review

Lincoln Financial Group is an A rated (Excellent) insurer founded in 1905 in Fort Wayne, Indiana, with the life business written through The Lincoln National Life Insurance Company. It is best known for TermAccel, a lab-free accelerated underwriting term product, the LifeElements term series, and a deep bench of universal, indexed, and variable universal life products used in estate and business planning.

Prudential Life Insurance Review

Prudential Financial is an A+ rated (Superior) insurer founded in 1875 in Newark, New Jersey, writing individual life through Pruco Life Insurance Company. Prudential is the carrier brokers turn to for complex health histories: it is known for favorable treatment of well-managed chronic conditions, was the first major U.S. carrier to underwrite applicants living with HIV, and famously offers non-smoker rates to occasional cigar smokers who test nicotine-free.

Principal Life Insurance Review - Exited Retail in 2021

Principal Financial Group, the A+ rated Des Moines insurer founded in 1879, no longer sells individual life insurance to retail consumers. After a 2021 strategic review, Principal exited the U.S. retail consumer life market to focus on retirement plans, asset management, and business-market insurance such as key person and buy-sell coverage. Existing retail policies remain in force and serviced. Business owners can still buy Principal life products through the business channel.

SBLI Life Insurance Review

SBLI (The Savings Bank Mutual Life Insurance Company of Massachusetts) is a mutual insurer founded in 1907 through the efforts of future Supreme Court Justice Louis Brandeis to give working families honest, low-cost life insurance. That mission still defines it: SBLI concentrates on competitively priced level term with an accelerated underwriting program that lets many applicants skip the medical exam, plus whole life for permanent needs.

TruStage Life Insurance Review

TruStage is the consumer brand of CMFG Life Insurance Company, an A rated (Excellent) insurer founded in 1935 as CUNA Mutual to serve credit union members and rebranded TruStage in 2023. It sells simplified term and whole life directly online with no medical exam on most products, plus guaranteed acceptance whole life. Face amounts are modest and pricing reflects the convenience, making TruStage best for smaller, fast policies rather than large family coverage.

Fidelity Life Review - RAPIDecision Term, Now Part of iA

Fidelity Life Association, the Chicago-area insurer founded in 1896 and known for its RAPIDecision product family, became part of Canada's iA Financial Group through the 2024 acquisition of its parent, Vericity. RAPIDecision term issues quickly with partial coverage up front, a distinctive hybrid: a portion of the death benefit starts immediately while the remainder can depend on completing underwriting. It fits shoppers who want coverage in force fast.

John Hancock Life Insurance Review

John Hancock is an A+ rated (Superior) life insurance company founded in 1862 in Boston and owned by Canada-based Manulife since 2004. Its signature feature is the Vitality wellness program, which discounts premiums and pays rewards for healthy behavior, and its Aspire program is purpose-built for people living with diabetes. John Hancock sells term, universal life, indexed UL, and variable UL.

Transamerica Life Insurance Review

Transamerica is an A+ rated (Superior) life insurance company founded in 1904 in San Francisco and now part of the Aegon group. It is one of the highest-volume term life carriers in the United States, best known for its Trendsetter term series with living benefits, competitive final expense whole life, and indexed universal life. Transamerica fits budget-focused term shoppers and applicants who want living benefit riders without a premium surcharge.

Kemper Life Insurance Review - Small Whole Life Policies

Kemper Corporation remains active in life insurance through its Kemper Life business, even after exiting its preferred home and auto lines in 2023. Kemper Life descends from the home service tradition: small whole life policies aimed at working families, historically sold and serviced by local agents. Coverage amounts are modest and per-dollar pricing is high compared with term, so the products fit final expense needs more than income replacement.

Voya Life Insurance Review - Exited Individual Life

Voya Financial, the retirement and benefits company formerly known as ING U.S., no longer sells individual life insurance. It stopped new individual life sales in 2019 and completed the sale of its in-force individual life block to Resolution Life in 2021. Existing Voya and legacy ING/ReliaStar policies remain fully in force and are administered through Resolution Life. Shoppers looking for coverage today should compare current top-rated carriers.

Costco Life Insurance Review - Protective Member Program

Costco's life insurance offering has been a member benefit program providing term life insurance through Protective Life, with pricing perks for Executive members. The coverage itself is standard Protective term, a strong, competitively priced product, with the Costco wrapper adding member conveniences. Program availability and terms can change, so members should verify current details through Costco Services, and every shopper should still compare two or three carriers before buying.

Liberty Bankers Life Review - Final Expense and Annuities

Liberty Bankers Life Insurance Company, headquartered in Dallas, is a growing insurer focused on simplified-issue final expense whole life and fixed annuities sold through independent agents. Its final expense line uses tiered acceptance so applicants with tougher health histories still find an offer, and its SIMPL-style simplified products emphasize fast, no-exam decisions.

Fabric by Gerber Life Review - Term Life for Parents

Fabric by Gerber Life is a digital life insurance brand aimed squarely at young parents, offering term policies with accelerated no-exam underwriting for qualifying applicants, plus free extras like online wills and family finance tools. Policies are issued within the Gerber Life family, part of Western & Southern Financial Group. Fabric fits busy parents who want solid term coverage and estate basics handled in one sitting.

Columbian Mutual Life Review - Acquired by JAB in 2025

Columbian Mutual Life Insurance Company, a New York insurer with roots to 1882 known for final expense and simplified-issue coverage, entered rehabilitation under the New York regulator after financial strain, and in November 2025 JAB Insurance agreed to acquire Columbian and its subsidiary, taking the company out of rehabilitation. Existing policies continue under regulatory protection. Final expense shoppers today should compare active specialists.

Genworth Life Insurance Review - No New Policies

Genworth Financial no longer sells life insurance. The company suspended new sales of traditional life insurance products in 2016 and wound down its remaining life and annuity sales in the years that followed, refocusing on long-term care insurance and its Enact mortgage insurance business. Existing Genworth life policies remain in force and continue to be serviced, but shoppers looking for coverage today need to compare active carriers.

MetLife Life Insurance Review - Individual Sales Ended

MetLife, founded in 1868 and one of the most recognizable names in American insurance, no longer sells individual life insurance to consumers. It spun off its U.S. retail business as Brighthouse Financial in 2017; existing retail policies are administered by Brighthouse, while MetLife continues to be a leader in group life insurance offered through employers. Shoppers who come looking for MetLife individual coverage today should compare current top-rated carriers instead.

Colonial Penn Life Insurance Review

Colonial Penn is an A rated (Excellent) life insurer founded in 1968 in Philadelphia and owned by CNO Financial Group. It is best known for the heavily televised $9.95 per unit guaranteed acceptance whole life program for ages 50 to 85, which asks no health questions but pays a graded benefit in the first two years. The catch every shopper should understand: a unit is not a fixed amount of coverage, and the same $9.95 buys less coverage the older you are.

World Financial Group Review - How the WFG Model Works

World Financial Group (WFG) is not an insurance company: it is a Transamerica-owned distribution agency whose associates sell life insurance and financial products, frequently indexed universal life, through a multi-level marketing structure. The policies WFG sells are real, issued by Transamerica and partner carriers, but the recruiting-driven model and IUL-heavy sales mix mean buyers should compare independent quotes and scrutinize illustrations before signing.

Nassau Financial Review - Annuities and Phoenix Legacy

Nassau Financial Group, founded in 2015 and headquartered in Hartford, Connecticut, is best understood in two parts: a growing fixed annuity business sold through agents, and the servicing home of legacy life insurance blocks, most notably the former Phoenix Companies policies it acquired. Consumers encounter Nassau either as annuity shoppers or as holders of older Phoenix-era life policies now serviced under the Nassau name.

William Penn Life Insurance Review - Banner's NY Sister

William Penn Life Insurance Company of New York is the New York-licensed carrier of Legal & General America and the sister company of Banner Life. Because New York's insurance regulations require a separately licensed entity, New Yorkers who want Banner's famously sharp term pricing buy the equivalent policies through William Penn. Products mirror the Banner shelf: competitively priced OPTerm level term with conversion options.

National Western Life Review - Now Part of Prosperity

National Western Life, the Austin, Texas insurer founded in 1956 and long controlled by the Moody family, was acquired by Prosperity Life Group in an all-cash merger valued at about $1.9 billion, completed in July 2024. The company's life insurance and annuity obligations continue under Prosperity's ownership. National Western historically emphasized annuities and universal life, with international life business as a distinctive niche.

Bestow Life Insurance Review - No Longer Selling Policies

Bestow, once a leading direct-to-consumer no-exam term startup, no longer sells life insurance to the public. The company pivoted to providing underwriting and policy technology to insurers. Term policies Bestow sold were issued by North American Company for Life and Health (a Sammons company) and remain fully in force. Shoppers who liked Bestow's instant no-exam experience have strong current alternatives, led by Ethos.

Sagicor Life Insurance Review - Product Lineup Changes

Sagicor Life Insurance Company, the U.S. arm of the Caribbean-based Sagicor Financial group, remains in business but discontinued the products this review originally covered: its Sage Term with instant Accelewriting no-exam underwriting, its universal life, and its no-exam whole life. Existing policies remain in force. Shoppers drawn to Sagicor's fast no-exam underwriting should compare current alternatives such as Ethos and Corebridge Quick Issue.

Sentinel Security Life Review - Final Expense Specialist

Sentinel Security Life Insurance Company, founded in 1948 in Salt Lake City by funeral directors, is a senior-market specialist selling final expense whole life, Medicare supplement plans, and fixed annuities through independent agents. Its New Vantage final expense line uses tiered acceptance so tougher health histories still find offers. Shoppers should verify the carrier's current financial strength rating as part of any purchase decision.

American Amicable Life Insurance Review - No-Exam Term

American Amicable is a Waco, Texas insurer with roots to 1910 that specializes in simplified-issue products sold through independent agents: no-exam term (including its Term Made Simple line), final expense whole life, and mortgage protection coverage. Underwriting relies on health questions plus database checks, making it a practical placement for applicants who want to skip the exam or carry moderate health histories.

Allstate Life Insurance Review - Sold to Everlake in 2021

Allstate, famous for auto and home coverage, no longer underwrites its own life insurance. It sold Allstate Life Insurance Company and related annuity businesses to Blackstone-managed entities in 2021, and those operations were renamed Everlake Life. Existing Allstate life policies remain in force and are serviced by Everlake, while Allstate agents today refer life shoppers to third-party carriers.

Prosperity Life Group Review - S.USA and Shenandoah Life

Prosperity Life Group is an insurance holding organization whose carriers include S.USA Life Insurance Company and Shenandoah Life, known for simplified-issue term and final expense whole life sold largely through independent agents. The group substantially increased its scale by acquiring National Western Life in a $1.9 billion merger completed in July 2024. Prosperity products suit shoppers who want simplified underwriting at modest face amounts.

Life Insurance With Epilepsy - Rates and Approval Guide

You can qualify for life insurance with epilepsy, and you will not be automatically declined. Underwriters price epilepsy on four factors: the type of seizures, how frequent and recent they are, whether the cause is idiopathic or symptomatic of another condition, and how consistently you follow your treatment plan. Applicants who have been seizure-free for two or more years on stable medication can approach Standard rates, while recent or frequent seizures lead to table ratings, and simplified or guaranteed issue policies backstop the harder cases.

Life Insurance for Diabetics - Type 1 and Type 2 Rates

You can get life insurance with diabetes, including type 1 and type 2. Well-controlled type 2 diabetics with a recent A1C under about 7.5 often qualify for Standard rates, type 1 diabetics typically receive Standard to table-rated offers depending on control and complications, and guaranteed issue coverage is available to anyone the traditional market declines. Because diabetic underwriting varies more between carriers than almost any other condition, comparing multiple insurers is the single highest-impact step.

Life Insurance for People With HIV - Coverage Options

People living with HIV can qualify for life insurance in the United States. A small but growing number of carriers now offer fully underwritten term and permanent policies to applicants with well-managed HIV, generally meaning consistent antiretroviral therapy, an undetectable viral load, and stable CD4 counts. Everyone else retains two no-health-question paths: guaranteed issue life insurance and employer group coverage. Disclosure is mandatory when asked; misrepresenting HIV status can void a policy during the contestability period.

Life Insurance for Overweight People - High BMI Rates

Being overweight does not stop you from getting life insurance. Carriers price weight using height-and-weight build charts rather than BMI alone, and most overweight applicants land between Standard rates and a few table ratings, each adding roughly 25 percent to the premium. Outright declines for weight alone are rare and generally limited to the most severe cases. Quitting nicotine, regular doctor visits, documented weight loss, and no-exam alternatives all improve the outcome.

Life Insurance After Retirement - Do Retirees Need It?

Most retirees no longer need life insurance once paychecks stop and children are independent, but four exceptions matter: a spouse who depends on your pension or Social Security income, outstanding debt such as a mortgage, estate liquidity and final expenses, and a pension election without a survivor benefit. Premiums rise steeply with age, so the decision is really a needs test: if nobody would suffer financially from your death, the premium usually serves you better elsewhere; if one of the four gaps applies, right-sized coverage still earns its keep.

Life Insurance for Smokers - Cigarette, Cigar, Vape Rates

Smokers typically pay 2 to 3 times more for life insurance than non-smokers, but the details matter enormously. Cigarettes, vaping, and chewing tobacco are usually priced at smoker rates, while occasional cigar smokers can qualify for non-smoker rates at select carriers if they test nicotine-free. Quitting changes everything: 12 months tobacco-free earns non-smoker rates at many carriers, and the best classes open up after 3 to 5 years. Because tobacco rules vary more between insurers than almost any other factor, carrier selection is the difference between overpaying and a fair price.

Sleep Apnea Life Insurance - Rates With CPAP Treatment

Sleep apnea does not automatically raise your life insurance rates. Mild apnea treated with documented CPAP compliance can qualify for Standard rates and sometimes better, moderate cases typically land at Standard to mild table ratings, and severe or untreated apnea leads to heavier ratings or a postponement until treatment is established. Completing the recommended sleep study and demonstrating consistent treatment are the two decisive moves an apnea applicant controls.

Life Insurance for Cancer Patients and Survivors

Both cancer patients and cancer survivors can get life insurance; the right product depends on where you are in treatment. During active treatment, guaranteed issue policies (no health questions, 2-year graded death benefit) and employer group coverage are the realistic options. After treatment ends, traditional term and permanent policies become available following a waiting period of roughly 1 to 10 years that varies by cancer type, stage, and treatment outcome. Some low-risk cancers, such as basal cell skin cancer, are insurable almost immediately.

Life Insurance With Bipolar Disorder or Schizophrenia

Many people with bipolar disorder or schizophrenia can still qualify for life insurance. Underwriters price these conditions on stability: consistent treatment, medication compliance, hospitalization history, work status, and time since the last acute episode. Long-stable, well-managed cases can reach Standard rates, moderate histories receive table-rated offers, and graded death benefit whole life plus guaranteed issue policies guarantee a path to coverage for histories that traditional underwriting declines.

Life Insurance With Depression or Anxiety - Best Rates

A depression or anxiety diagnosis does not prevent you from getting life insurance. Applicants with mild, well-managed symptoms controlled by therapy or a single stable medication routinely qualify for Standard rates, and lenient carriers will consider better classes. Severity is what moves pricing: hospitalizations, multiple medications, missed work or disability claims, and any history of suicidal ideation push offers into table ratings, while simplified issue and guaranteed issue policies remain available for tougher histories.

Decreasing Term Life Insurance: How It Works and Cost

Decreasing term life insurance is a term life policy whose death benefit drops on a fixed schedule over the life of the policy, typically aligned with a declining obligation like a mortgage payoff or business loan. Premiums are usually level, not decreasing, despite the falling death benefit. Decreasing term is much less common in the U.S. retail market than level term because the premium savings are typically small and the buyer is exposed to a coverage shortfall if the underlying obligation is paid down slower than the schedule assumes.