Quick answer

A buy-sell agreement funded with life insurance guarantees the money to buy out a deceased owner's share will exist the moment it is needed. In a cross-purchase plan, each owner buys a policy on the others; in an entity purchase plan, the business owns one policy per owner. Either way, surviving owners keep control, and the family receives fair value in cash instead of an ownership stake.

What are The benefits of a Buy-Sell Agreement funded by life insurance?

With a buy-sell agreement that is funded by life insurance, the company or the individual co-owners buy life insurance policies on the lives of each co-owner. Thus, if you died, the company or the co-owners would receive the death benefits from the insurance policies on your life.

What is a Buy-Sell Agreement With Life Insurance?

A buy-sell agreement is a legally binding agreement between the co-owners of a business. It is sometimes referred to as a buyout agreement.

A buy-sell agreement governs the situation if a co-owner dies, is forced to leave the business, or simply chooses to leave the business. It serves as a kind of prenuptial agreement between the business partners and/or shareholders of a company, sometimes called a “business will.”

How to Fund a Buy-Sell Agreement With Life Insurance?

With a buy-sell agreement that is funded by life insurance, the company or the individual co-owners buy life insurance policies on the lives of each co-owner.

Thus, if you died, the company or the co-owners would receive the death benefits from the insurance policies on your life.

Plus, your family would get a sum of cash as payment for your interest in the business. This provides financial support for them after your death and it also provides stability for the company.

What are the Types of Buy-Sell Agreements?

Buy-sell agreements can take different forms, but the two typical structures are cross-purchase plans and entity redemption plans, with a hybrid version also available as a third possible option.

Cross Purchase Plan

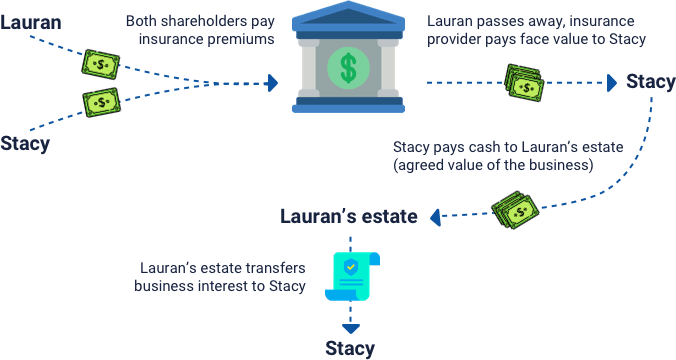

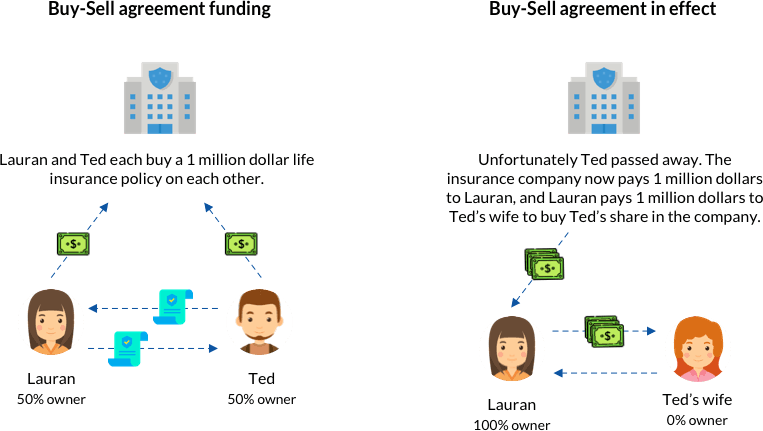

In a cross purchase plan, each owner purchases a life insurance policy on the other owner or owners. Each owner pays the annual premiums on the policy they own and each is the beneficiary of the policy. When an owner dies, the surviving owners use the death benefit to purchase the deceased owner’s share of the business. If there are a large number of owners of the business, multiple policies must be purchased by each owner.

Example

In the following Cross Purchase Plan example, the business is valued at 2 million dollars, and has 2 owners, Lauran and Ted. Each owner holds 50% of the company.

Entity Redemption Plan

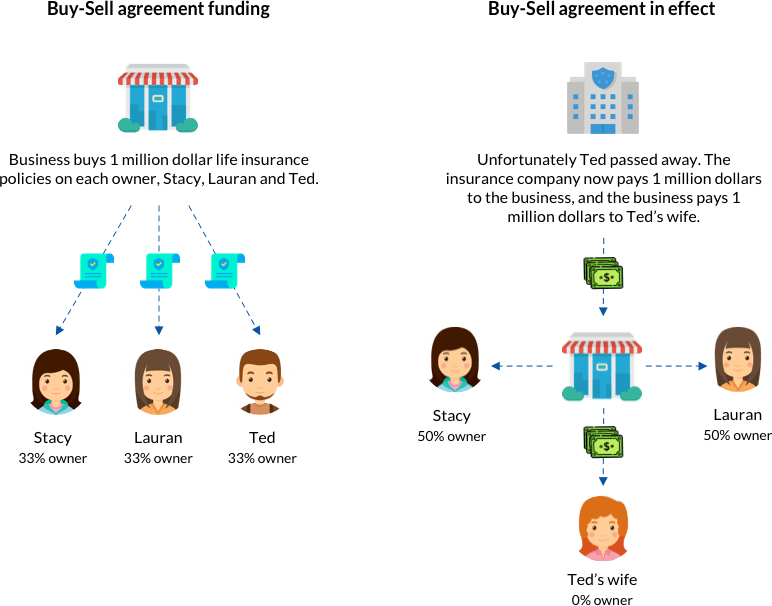

In an entity redemption plan, each owner has an arrangement with the business for the sale of their respective interests to the business. The business purchases separate life insurance policies on the lives of the owners. The business pays the premiums. And the business is the owner and beneficiary of the policy. When an owner dies, his or her share of company stock will pass to his or her heirs or estate, and the company may purchase them with the proceeds from the life insurance policy.

Example

In the following Entity Redemption Plan example, the business is valued at 3 million dollars, and has 3 owners, Stacy, Lauran and Ted. Each owner holds 33% of the company.

Hybrid Plan

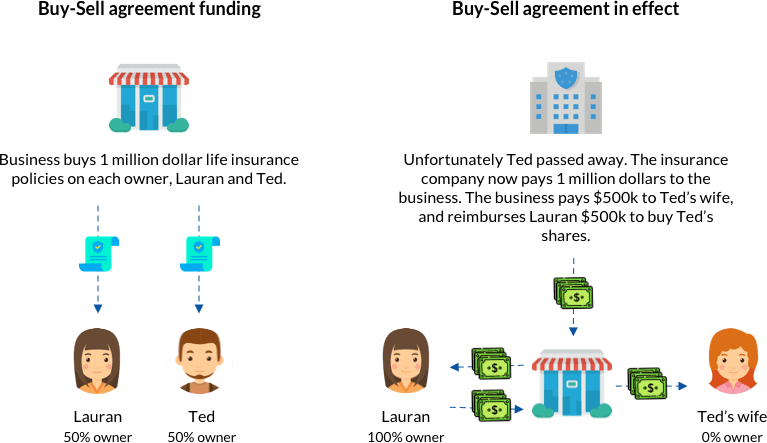

A hybrid plan, as you might have guessed, combines the first two types of buy-sell agreements: cross purchase and entity redemption. Typically, the owner is required to offer his or her interest to the entity. If the entity declines or cannot make the purchase, however, other co-owners or partners can purchase the shares. This type of arrangement may also allow certain employees, like longtime company officials, to purchase the interest.

Example

In the following Hybrid Plan example, the business is valued at 1 million dollars, and has 2 owners, Lauran and Ted. Each owner holds 50% of the company.

Potential Benefits

No matter what kind of business you are involved in, a corporation, a partnership, an LLC, or even a proprietorship, you should strongly consider a buy-sell agreement.

Business specialists and financial planners often recommend life insurance to ensure that a buy-sell agreement is funded properly, guaranteeing that there will be money available should the buy-sell event become a reality.

Plus, the proceeds are usually paid quickly after your death. And if sufficient cash values are available within the policies, the funds can be accessed to purchase your interest in the business if you retire or become disabled. Additionally, the life insurance policy proceeds are typically free from income tax regardless of who owns the policy.

Tax Considerations

There are several tax considerations that should be made when funding a buy-sell agreement with life insurance. As previously mentioned, the death proceeds are free from income tax. If the business is a C corporation, however, the death proceeds may be subject to the alternative minimum tax (AMT).

There are other tax considerations:

- The premiums used to fund a buy-sell agreement are not tax deductible.

- The payment of premiums made by a business, where the shareholder or the owner is the insured, are not considered taxable income.

- In a cross purchase agreement, the cash value of the policies owned by the deceased on the other shareholder’s lives is considered to be in the deceased’s estate. The policies owned by the other shareholder’s on the deceased’s life are not considered in the decedent’s estate, though.

Consult with your legal or tax advisor for answers to specific tax questions regarding a buy-sell agreement.

Take Care of Your Business and Your Family

A buy-sell agreement funded with life insurance will give you the confidence that your business and your family will be taken care of in your absence. Plus, the cost is small compared to the benefits.

Get a Buy-Sell Agreement Funded by Life Insurance

A buy-sell agreement funded with life insurance will give you the confidence that your business and your family will be taken care of in your absence. Plus, the cost is small compared to the benefits.

Below is a list of companies that provide policies for buy-sell agreements.

Ready to shop for life insurance? Start here