The Insurancy Blog

Insights that make insurance simple

264 expert guides, company reviews and original studies. Written and reviewed by licensed insurance agents.

Category:All articles264

Featured

FeaturedMore Guides

14 Steps to Settle Debt With a Creditor or Debt Collector

Overdue debt causes real stress, and calls from debt collectors can feel overwhelming. Attorney Lyle Solomon walks through 14 practical steps for settling debt with a creditor or collector: keep a collections log, validate the debt before paying, get every agreement in writing, and know the FDCPA protections that limit what collectors can do.

Lyle Solomon•Updated Jul 2026

Read article› More Guides

More GuidesEnd of Life: A Grief Support Resource Guide

There is nothing in life harder than the death of a loved one. Grief is real, with both mental and physical symptoms, and even the very worst grief is survivable. This resource guide collects vetted links for coping with grief day to day, recognizing complicated grief, finding support groups, and supporting children and families through specific kinds of loss.

Brian Greenberg•Updated Jul 2026

More Guides

More GuidesHealth Resources for End-of-Life Care

End of life looks different for everyone, which makes planning ahead feel uncertain. This guide collects trusted resources for every stage: elder care and healthy aging, hospice and palliative care, advance directives, locating life insurance policies and filing claims, and grief support for the whole family.

Brian Greenberg•Updated Jul 2026

Studies & Surveys

Studies & SurveysBreast Cancer Statistics - Key Facts and Survival Rates

The American Cancer Society estimates 316,950 new invasive breast cancer cases and 42,170 deaths among US women in 2025. Median age at diagnosis is 62, incidence has risen about 1% per year from 2012 to 2021, and death rates continue a long decline thanks to screening and better treatment.

Brian Greenberg•Updated Jul 2026

Studies & Surveys

Studies & SurveysBuyer Trust and Influence Study 2024 - Key Findings

Insurancy asked nearly 2,400 US respondents about their online browsing and purchasing habits to understand what builds buying trust. The study covers how reviews, social proof, search behavior, and brand reputation shape the modern path to purchase.

Brian Greenberg•Updated Jul 2026

Studies & Surveys

Studies & SurveysCOVID-19 and Life Insurance Survey - Consumer Outlook

Insurancy's COVID-19 and life insurance survey of 1,500 people found nearly half already had a policy and about 70% said the pandemic did not change their outlook on coverage. Insurers now ask about COVID-19 in applications, and a positive test can mean a 30-to-60-day waiting period before a new policy is issued.

Brian Greenberg•Updated Jul 2026

Studies & Surveys

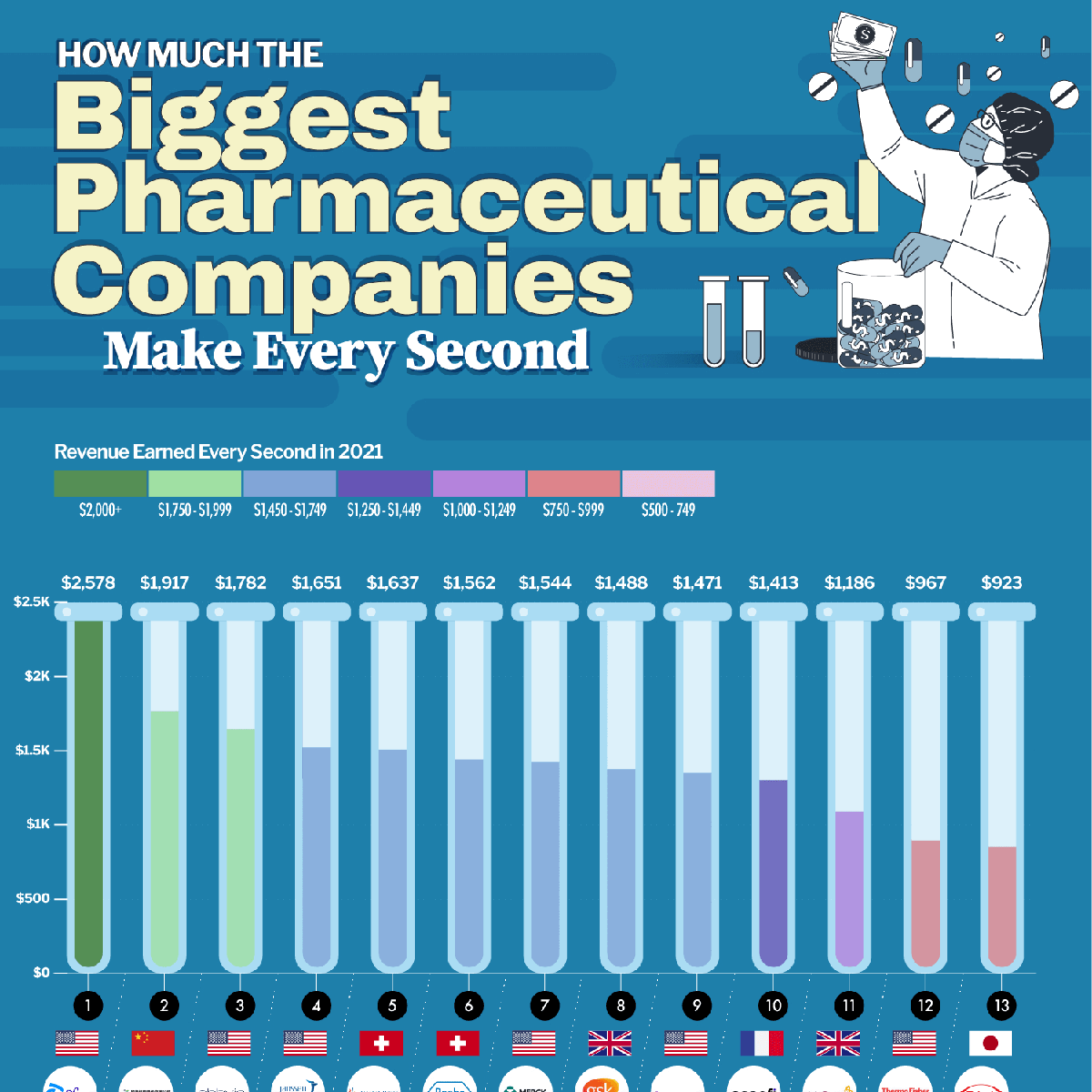

Studies & SurveysHow Much the Biggest Pharma Companies Make Every Second

Insurancy broke down the annual revenue of the 25 biggest pharmaceutical companies into revenue per second. Pfizer topped the 2021 ranking at $2,578 earned every second, and the 2024 update shows Johnson & Johnson leading at roughly $2,816 per second based on full-year 2024 reports.

Brian Greenberg•Updated Jul 2026

Studies & Surveys

Studies & SurveysInsurtech Survey - Fitness Trackers and Life Insurance

Insurancy's insurtech survey of roughly 1,000 US respondents found 77% are uncomfortable with life insurance premiums that fluctuate based on yearly physicals, and 59% refuse to wear a fitness tracker that reports to insurers - even for a better rate. Younger respondents were the most resistant, complicating the industry's wearables push.

Brian Greenberg•Updated Jul 2026

Studies & Surveys

Studies & SurveysInvestment Trends Study 2025 - Investor Statistics

Insurancy's investment trends study surveys how Americans invest: online apps, cryptocurrency, internet investing, robo-advisors, and the differences in how men and women approach the market.

Brian Greenberg•Updated Jul 2026

Studies & SurveysLife Insurance and COVID-19 Study - 2024 Findings

Insurancy's life insurance and COVID-19 study found 48.2% of respondents own a personal policy, interest in buying coverage rose slightly during the pandemic, and 3 in 4 people do not believe COVID-19 will be treated as a pre-existing condition. Concerns about rising rates were common, making early application the practical takeaway.

Brian Greenberg•Updated Jul 2026

Studies & Surveys

Studies & SurveysLife Insurance Statistics 2026 - US Industry Facts

About 51% of American adults own life insurance according to LIMRA's 2025 Insurance Barometer Study, and ownership has drifted down from 63% in 2011. This report combines Insurancy's own consumer research with industry data on why people buy coverage, how they shop, and which companies write the most premiums.

Brian Greenberg•Updated Jul 2026

Studies & Surveys

Studies & SurveysLife Insurance Consumer Report 2025 - Key Findings

Insurancy's Life Insurance Consumer Report finds Gen X is the age group most likely to own life insurance and Gen Z the least likely, while marriage and children both raise ownership sharply. Notably, 70% of respondents now estimate the cost of life insurance correctly, challenging the long-held industry belief that consumers dramatically overestimate prices.

Brian Greenberg•Updated Jul 2026

Studies & Surveys

Studies & SurveysLife Insurance Industry Trends Survey 2022 - Results

Insurancy's life insurance industry trends survey found consumers cool on insurtech: 77% reject fluctuating premiums tied to physicals, 62% are uneasy about AI in the buying process, only 7% would share DNA data, and 78% still prefer buying from a local agent. Gen Z stands apart, ranking retailers like Costco and Amazon above online agencies.

Brian Greenberg•Updated Jul 2026

Studies & Surveys

Studies & SurveysOnline Shopping and E-commerce Statistics 2024 Study

Insurancy surveyed 2,400 US respondents about their online research and purchasing habits. The e-commerce study covers how shoppers use reviews and search, how mobile changes buying behavior, and what ultimately drives online purchases.

Brian Greenberg•Updated Jul 2026

Studies & Surveys

Studies & SurveysWhat Is Bereavement and End-of-Life Support?

Bereavement is the period of grief and mourning after the death of a loved one. Grief affects everyone differently, from anticipatory grief before a death to complicated grief that lingers. This guide explains the types and manifestations of grief and collects vetted resources for supporting the bereaved - and the end-of-life nurses who care for dying patients.

Brian Greenberg•Updated Jul 2026

Car Insurance

Car Insurance6-Month vs 12-Month Auto Insurance - Which Is Cheaper?

A 6-month auto insurance policy costs about the same per month as a 12-month policy - the real difference is flexibility versus rate lock. A 6-month term lets you re-shop or switch carriers twice a year, while a 12-month term locks your rate for a full year, which helps if you get a ticket or file a claim mid-policy. Full-coverage 12-month premiums for a typical driver run about $1,400 to $2,580.

Brian Greenberg•Updated Jul 2026

Car Insurance

Car InsuranceArizona Commercial Auto Insurance - Requirements and Rates

Arizona commercial auto insurance covers vehicles used for business purposes and carries the same 25/50/15 minimum liability limits as personal policies, though most businesses need considerably higher limits. Any car, truck, van, or SUV used for business counts as a commercial vehicle, and personal policies typically exclude business-use claims.

Brian Greenberg•Updated Jul 2026

Car Insurance

Car InsuranceAuto Insurance for a Rebuilt Title Car - What to Expect

You can get auto insurance on a car with a rebuilt title, but expect extra steps: most states require an official inspection, and many insurers offer only liability coverage on rebuilt titles. Average premiums run about $2,422 a year for full coverage and $1,244 for liability-only, a bit more than a comparable clean-title car.

Brian Greenberg•Updated Jul 2026

Car Insurance

Car InsuranceCar Insurance Without a License - How to Get Covered

You can get car insurance without a driver's license, usually by listing a licensed household member or caregiver as the primary driver and excluding yourself. Common reasons include owning a car someone else drives, keeping a stored or classic car covered, and protecting a vehicle for a teen or elderly relative.

Brian Greenberg•Updated Jul 2026

Car Insurance

Car InsuranceBest Car Insurance for 16-Year-Olds - Rates and Discounts

The best car insurance for a 16-year-old is almost always to add them as a driver on a parent policy, which typically costs 40 to 60 percent less than a stand-alone policy for the same teen. Top insurers for teens include GEICO, State Farm, Progressive, and USAA (for military families), with good-student and driver-training discounts often stacking to 25 to 30 percent off.

Brian Greenberg•Updated Jul 2026

Car Insurance

Car InsuranceBest Car Insurance for 17-Year-Olds - Cost and Discounts

The best car insurance for a 17-year-old is typically to stay on a parent policy as a listed driver, where the shared premium is roughly half the cost of a stand-alone teen policy. Nationally the cheapest carriers for 17-year-olds are USAA (military only), GEICO, State Farm, and Erie in the states where it operates. Good-student and defensive-driving discounts can cut 15 to 25 percent off the premium.

Brian Greenberg•Updated Jul 2026

Car Insurance

Car InsuranceBest Car Insurance for 18-Year-Olds - Cost and Discounts

At 18, most drivers can legally sign their own auto policy, but the best car insurance for an 18-year-old is still typically to stay on a parent policy. A stand-alone policy for an 18-year-old averages about $3,600 to $5,200 a year, while adding an 18-year-old to a parent policy raises the family premium by roughly $1,800 to $2,400. Good-student and telematics discounts cut both by 15 to 25 percent.

Brian Greenberg•Updated Jul 2026

Car Insurance

Car InsuranceBest Car Insurance for 19-Year-Olds - Rates and Savings

A 19-year-old typically pays roughly half what a 16-year-old pays for car insurance, but still 2 to 3 times what a 30-year-old pays. The best carriers for 19-year-olds nationally are GEICO, State Farm, Progressive, and USAA for military families. Good-student, student-away-at-school, and telematics (usage-based) discounts can cut the premium another 15 to 25 percent.

Brian Greenberg•Updated Jul 2026

Car Insurance

Car InsuranceBest Car Insurance for 20-Year-Olds - Rates and Discounts

A 20-year-old typically pays $2,400 to $3,600 a year for a stand-alone auto policy, or about $1,200 to $1,800 in additional premium if added to a parent policy. Cheapest carriers nationally for 20-year-olds include GEICO, USAA, Erie, and State Farm. Good-student, defensive-driving, telematics, and multi-line (bundling with renters) discounts can stack to 20 to 30 percent off.

Brian Greenberg•Updated Jul 2026

Car Insurance

Car InsuranceBest Car Insurance for 21-Year-Olds - Rates and Discounts

At 21, car insurance rates drop sharply as most carriers move drivers out of the youthful bracket. A 21-year-old typically pays $1,900 to $2,900 a year for a stand-alone policy. Cheapest carriers for 21-year-olds nationally are USAA (military only), GEICO, Erie, and State Farm. Good-student, defensive-driving, telematics, and renters or homeowners bundling discounts can cut premium another 20 to 25 percent.

Brian Greenberg•Updated Jul 2026