Quick answer

You do not need an employer to get group life insurance: associations and membership groups offer it too. Joining a professional, fraternal, or membership association can unlock group term or group whole life plans with simplified underwriting and group pricing. It is a practical route for people without workplace coverage or those supplementing it, though group coverage alone is rarely enough for a family's full needs.

Best Associations to Join for Group Life Insurance

Joining an association that offers life insurance to its members can provide an affordable and convenient solution for individuals who do not have access to employer-provided group life insurance or want to supplement their existing coverage.

| Company | Info | Rating | Recommendation | Quote |

|---|---|---|---|---|

| Recommended. | ★★★★★ Brochure | Wellness Association of America. For those looking for coverage with no health questions. | Go |

| Recommended Has medical history questions. Coverage up to $100,000. Term life insurance. Additional member benefits. | ★★★★★ | Premier Business Association. For those looking for quick term coverage with limited questions to qualify. | Go |

What Is Group Life Insurance?

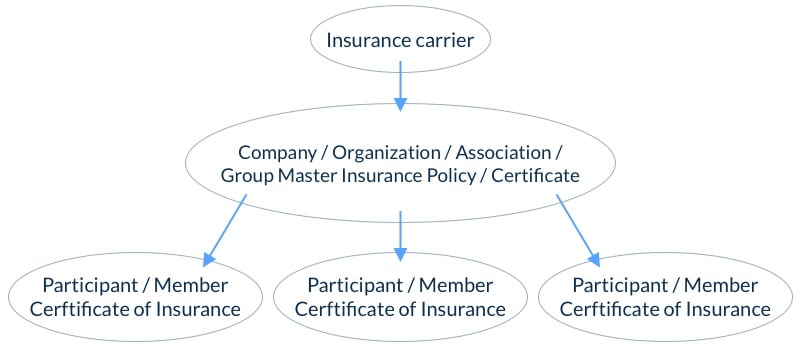

Group life insurance is a type of life insurance coverage in which a group is the master policyholder of an insurance contract, and certificates of insurance are issued to participating individual members.

These insurance policies are most commonly offered by employers to their employees as a free or optional benefit. Entities such as organizations, trade groups, and associations also can offer group life insurance to their members.

It is available to people of all ages, and there are few health questions, if any, that must be answered in order to qualify. Term and whole life policies may be available, depending on the group.

When Should You Get a Group Life Policy?

When coverage is offered for free

When group life coverage is offered as a free benefit - in this case, there is no reason to pass it up.

For inexpensive supplemental coverage

Group life insurance is a benefit and should not be the only life insurance coverage you have. It is recommended that you have individual life insurance, and a group life policy as additional coverage.

Since the risk of a claim is spread out among a large group, coverage costs are low for participants. Optional group coverage may or may not be a good financial decision. For those in good health, it is often cheaper to purchase an individual life insurance policy than to spend money on group coverage.

When you cannot qualify for individual life insurance

If you under 50 years of age and cannot qualify for individual life insurance, group coverage may be the only way to obtain life insurance.

Since there are few health questions that must be answered to qualify for group life coverage, this type of insurance is an option for people with health conditions such as:

- Cancer

- Schizophrenia

- Immune disorders

- Heart disease

- Diabetes

How to Join a Group or Association

There are many types of groups and they all have different requirements for becoming a member.

Some charge membership fees or have participation requirements for its members.

Some associations that offer the best group life insurance:

- Freelancers Union

- AARP

- Costco Insurance Marketplace

- Writers Guild of America West

- Small Business Service Bureau

- National Education Association

- Woman’s Life Insurance Society

- American College of Physicians

- Financial Planning Association

Another way to find potential groups/associations is a google search for membership life insurance benefit

Access to groups and associations is a way to get access to insurance products and rates that are not possible for individuals.

Things to ask before becoming a member of a group

- What are the requirements to become a member?

- What are the requirements to stay a member?

- Is the life insurance product portable?

- Who is the carrier issuing the insurance products?

- What is the financial rating of the insurance company?

- Can I see an illustration of the policy that shows the guaranteed premiums and coverage?

Group Life Insurance Pros and Cons

What we like

More affordable than traditional policies

The risk to the insurance company is spread out among many participants in group plans. Group life insurance is often free for qualifying employees and group members.

It’s easy to qualify for group insurance

Group life plans have few health questions to qualify. Some plans have no health questions. The more coverage you apply for, the more health questions.

Fast approval

Applications are one or two pages, and they are active when the policy is processed by the insurance company. How fast this happens depends on the group and insurance company issuing the certificates. If you apply online, your policy may be active the moment you sign and date the application.

Full coverage from day 1

group policies do not have waiting periods for the full coverage amount to be available to beneficiaries. Some final expense whole life policies have a two-year waiting period for the full coverage amount is available.

There is no need for a medical exam

Medical exams cost insurance companies money. For small group life plans, the risk to insurance companies is small, so exams are not required. Typically the application is the only requirement to qualify.

There is no financial history check

When coverage amounts are small, insurance companies do not run financial risk assessments. Risk assessments cost the insurance company money are not required. As you increase your coverage amount, the insurance company may require this qualification requirement.

There are no height and weight requirements

Individual life insurance policies use build charts as one of the factors in determining the cost of a policy. Group life plans don’t have health classes so there is no need for height and weight requirements.

What we don’t like

It’s possible to lose the coverage if

- You leave the company or group

- The group drops the benefit

- The company or group closes

You are not the owner of the policy

As with group life insurance offered through an employer, the association is the ultimate policyholder. The association holds the master policy, and issues certificates of insurance to its members. While a certificate of insurance is valid proof of having a life insurance policy, you are not the owner of the policy.

Premiums may increase

If the premiums aren’t guaranteed and the group experiences too many claims they can raise the premiums. Another way the premium could increase is if the plan offered is a “banded term policy in which the premiums increase every five years.

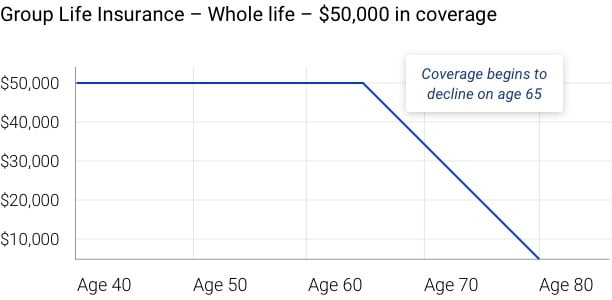

Coverage may decrease:

This happens when the premiums are guaranteed, but the coverage isn’t. As you age, the risk to the insurance company increases. When you reach a certain age, typically 60 years old, the coverage amount begins to decrease every year.

Coverage is less compared to traditional policies

Group life is easier to qualify for than fully underwritten individual policies. Since there are so few health questions, the insurance company lowers its risk by offering low amounts of coverage.

Difficult to service

The insurance company does not handle general services like updating billing or beneficiary changes. Instead, service is often handled by the master certificate holder. This can cause confusion when the plan administrator is not a licensed insurance agent.

How Does Group Term Life Insurance Work?

Group term policies with 5 year coverage periods. Every five years the cost of the coverage increases.

How Does Group Whole Life Insurance Work?

Group whole life policies with guaranteed level premiums where the coverage amount decreases after age 65.

Group Life Insurance Statistics

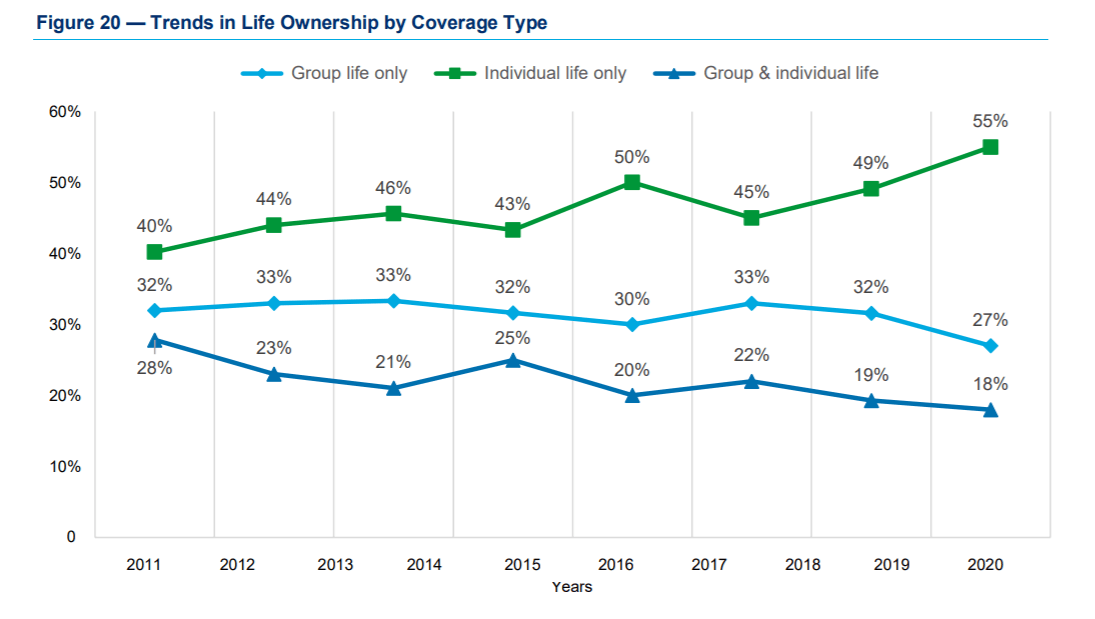

Group life insurance policies have been declining for the last decade

Depending on your personal situation, the pros can far outweigh the cons. Especially for individuals who would have a tough time qualifying for an individual life insurance policy, due to their health. Yet, group life insurance popularity has been declining for the last decade. Why?

source: 2020 Limra Insurance Barometer Study

This could be largely due to the fact that fewer employers are offering group life insurance through work. Many individuals aren’t aware that they can join a group or association that offers this type of insurance on their own.

Of individuals who have life insurance in general, 55% of people have an individually owned life insurance policy, which is still the most popular choice by far. One in four individuals (27%) have group life insurance only.

Lastly, 18% of people who have life insurance, have both an individual and group owned policy.

Join a Group

Join an association that offers life insurance to members.