Quick answer

Insurancy's life insurance industry trends survey found consumers cool on insurtech: 77% reject premiums that fluctuate with yearly physicals, 62% are uneasy about AI in the buying process, and only 7% would share DNA data for a discount. 78% still prefer buying from a local agent, though Gen Z stands apart - ranking retailers like Costco and Amazon above online agencies.

Key Statistics:

- 77% of respondents said they were uncomfortable having their premiums fluctuate based on their yearly physical results.

- 59% of overall respondents overall said they would not be willing to wear a fitness tracker and share their data with insurance companies for better rates.

- When offered the choice, only 7% of overall respondents said they would be comfortable providing their DNA testing information in exchange for better rates or premiums.

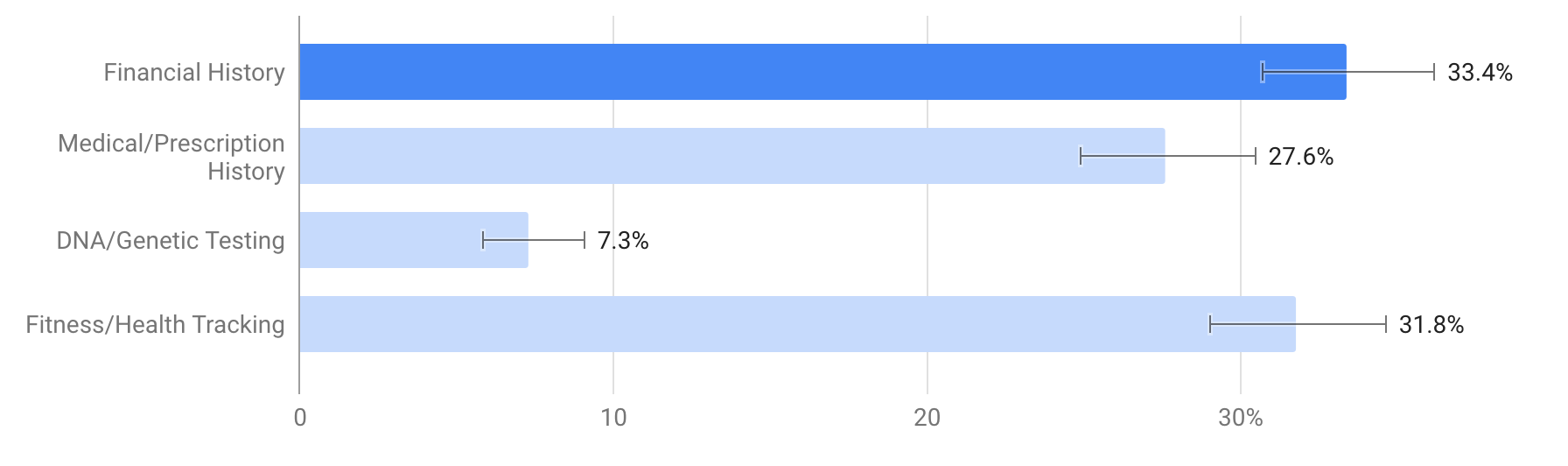

- Depending on age demographics, respondents were most comfortable providing either their financial history or fitness data when forced to choose, if it meant receiving better rates or premiums.

- 62% of respondents were uncomfortable with the idea of using AI in their insurance buying experience.

- 78% of respondents said they would feel most confident buying life insurance from a local agent versus a big box retailer or online agency.

- For Gen Z respondents, Costco, Walmart, and Amazon were more popular choices than online agencies.

Looking forward at the trends hitting the insurance world in 2022, they are setting the stage for some massive game-changers that stand to change the industry as we all know it. For national context, the Insurance Information Institute’s life insurance statistics and LIMRA’s ownership research track how these forces are playing out market-wide.

At large, this survey found that consumers were generally uncomfortable sharing sensitive information with insurance companies and dealing with AI-driven, automated underwriting processes. While consumers may not currently be receptive to these innovations, it is clear that the game-changers they power are here to stay.

Beyond these general findings, read our more detailed breakdowns for each question below and how each sets up these 2022 game-changers:

Would you be willing to have your life insurance premiums fluctuate based on the results of your yearly physical?

- 77% of respondents said they were uncomfortable having their premiums fluctuate based on their yearly physical results.

The results here point to a general discomfort that respondents felt about the idea of having their rate fluctuate along with their health data. Unlike with traditional life insurance policies where an agent quotes the insured for a standard rate, this kind of variable premium policy means that unhealthy lifestyles, as tracked through yearly physical data, would result in higher premiums.

On one hand, companies like John Hancock and Health IQ believe that variable premium policies are a game-changer that will help encourage healthier insureds over the long term. In reality, it stands to drive unhealthy people away from even considering a life insurance policy for fear of astronomical premiums or denial of coverage. It makes it clear that these policies only benefit those who are already healthy

This line of thinking also pulls back the curtain on how a significant portion of the US population is either underinsured or doesn’t think they’re insurable because of their health. While variable premium policies were created with the best intention, they are also widening the gap for people who really need the coverage, but can’t find it.

Would you be willing to wear a fitness tracker and submit reports to insurance companies if it means potentially receiving a better premium?

- 59% of overall respondents overall said they would not be willing to wear a fitness tracker and share their data with insurance companies for better rates.

- 54% of respondents aged 18-24 were unwilling to wear a fitness tracker and report data to insurance companies in exchange for receiving a potentially better premium.

Similar to their response toward fluctuating premiums, respondents weren’t exactly receptive to the idea of submitting their fitness data to dictate their insurance premiums. It’s another system that seems to favor the healthy and drive the wedge in further for unhealthy people.

But, the margin here is much smaller, and previous answers in this survey show that respondents may be more receptive to sharing this kind of information when offered a choice. John Hancock has seen success with their Vitality Program over the past few years, though it is still yet to be seen what effect making these interactive policies standard issue will have on their company. Coupled with the least negative response from Gen Z respondents, the use of fitness data may have some staying power in the future of insurance underwriting.

If you had to choose one, what background information source would you be most comfortable sharing with insurance companies to use when setting your rates/premiums?

- When offered the choice, only 7% of overall respondents said they would be comfortable providing their DNA testing information in exchange for better rates or premiums.

- Depending on age demographics, respondents were most comfortable providing either their financial history or fitness data when forced to choose, if it meant receiving better rates or premiums.

The even split between the data (financial, fitness, and medical data) consumers are willing to provide insurance companies to set their premiums shows, despite general apprehension, they’ll eventually give their information.

With future buying experiences based on automated underwriting, this is the information that is driving the processes many insurers are already using. While consumers may seem apprehensive about the ideas of AI or giving out sensitive information, they’ll wind up submitting at least one of these types of data. This is especially if it doesn’t appear to be too invasive and makes their experience more convenient.

As an abstract concept, consumers may not like giving up their information, but utilizing it is key to powering the agentless innovations across the industry and it shows no signs of slowing down. In the end, it will just take a little time for consumers to warm up to this kind of innovation as the new normal.

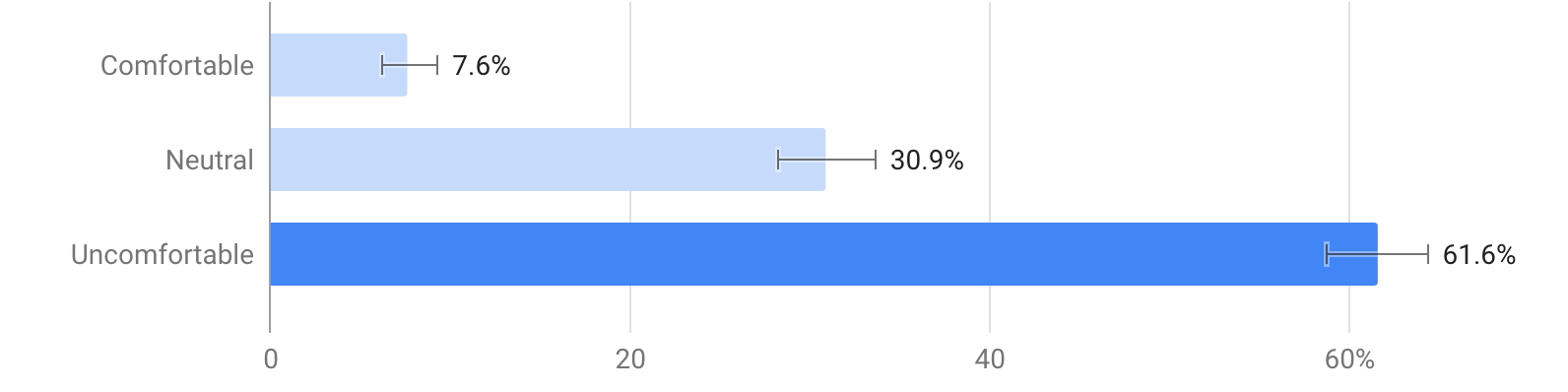

How comfortable would you feel buying an insurance policy with the help of an AI program versus a human agent?

- 62% of respondents were uncomfortable with the idea of using AI in their insurance buying experience.

Based on the results from this question, it is clear that the idea of using AI is still really unsettling to a lot of consumers. Taken in tandem with consumer’s preference for using a local agent, AI-powered automation may make insurance buying experiences seem more impersonal.

On the flipside of this AI apprehension, the implementation of agentless solutions opens up the insurance industry for more growth and change. It allows companies like Transamerica and MetLife to have incubators and investment arms, which allows them to innovate in preparation for incoming “market killer” competitors. This even allows insurers, like Principal and Assurity, to raise their coverage maximums as high as $1 million without medical exams. Just like in any other industry, it may take time for consumers to get used to the idea of using AI for insurance buying.

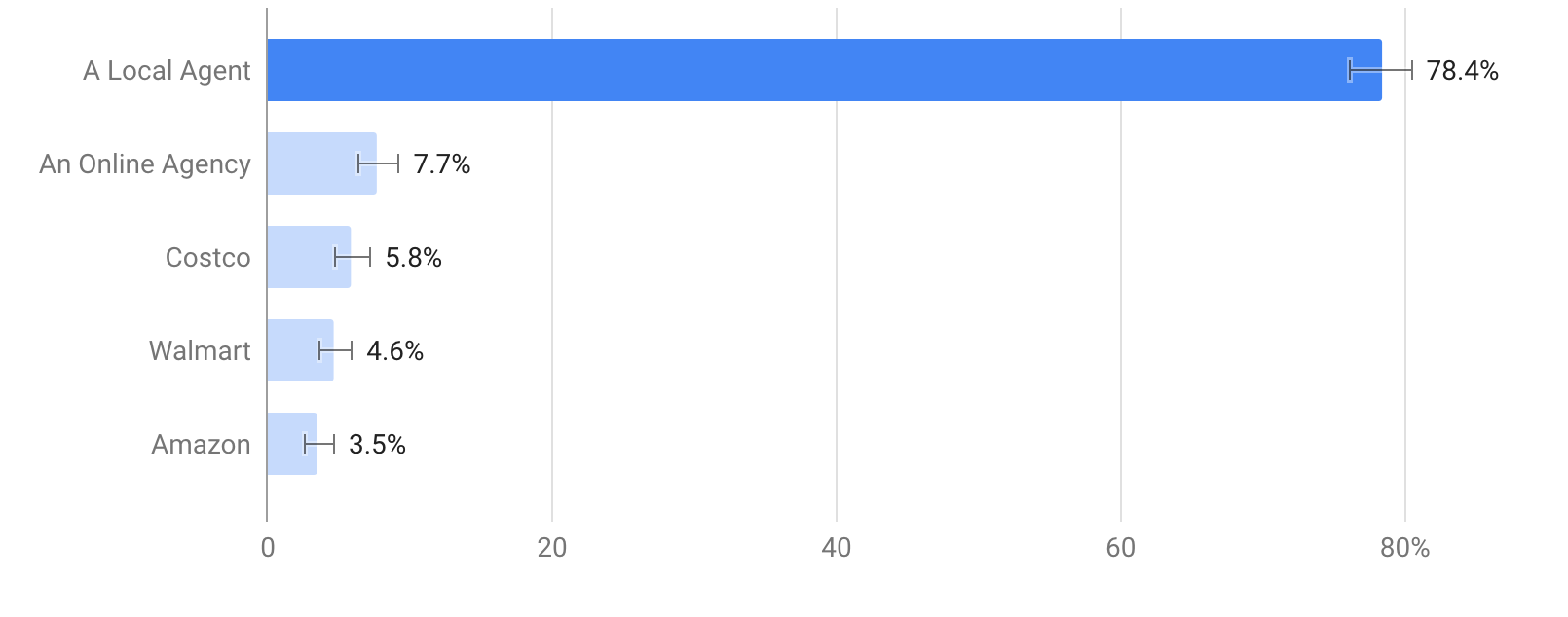

Where would you feel most confident buying a life insurance policy?

- 78% of respondents said they would feel most confident buying life insurance from a local agent versus a big box retailer or online agency.

- For Gen Z respondents, outside of a local agent, Costco, Walmart, and Amazon were more popular choices than online agencies, the overall second choice.

The popularity of local agents in this question illustrates consumer apprehension toward agentless solutions. Despite this, many insurers are still pursuing agentless solutions, cutting out many of the human elements of their processes in favor of convenience and cost-cutting.

Though they rank relatively low in our survey results, Costco, Amazon, and Walmart have all entered the insurance industry in one way or another in recent years. They stand to drastically change the way everyone in the insurance industry does business, which is why some consider them “market killers.”

To add even more credence to the potential of these “market killers,” for Gen Z respondents (aged 18-24), Costco, Walmart, and Amazon were all more popular options than an online agency, which was the overall second choice. As they were the only demographic who responded like this and will soon start buying insurance, this is clear evidence for why these established retailers and brands stand to be key forces in the insurance world moving forward.

- When offered the choice, only 7% of overall respondents said they would be comfortable providing their DNA testing information in exchange for better rates or premiums.

- Depending on age demographics, respondents were most comfortable providing either their financial history or fitness data when forced to choose, if it meant receiving better rates or premiums.

The even split between the data (financial, fitness, and medical data) consumers are willing to provide insurance companies to set their premiums shows, despite general apprehension, they’ll eventually give their information.

With future buying experiences based on automated underwriting, this is the information that is driving the processes many insurers are already using. While consumers may seem apprehensive about the ideas of AI or giving out sensitive information, they’ll wind up submitting at least one of these types of data. This is especially if it doesn’t appear to be too invasive and makes their experience more convenient.

As an abstract concept, consumers may not like giving up their information, but utilizing it is key to powering the agentless innovations across the industry and it shows no signs of slowing down. In the end, it will just take a little time for consumers to warm up to this kind of innovation as the new normal.

How comfortable would you feel buying an insurance policy with the help of an AI program versus a human agent?

- 62% of respondents were uncomfortable with the idea of using AI in their insurance buying experience.

Based on the results from this question, it is clear that the idea of using AI is still really unsettling to a lot of consumers. Taken in tandem with consumer’s preference for using a local agent, AI-powered automation may make insurance buying experiences seem more impersonal.

On the flipside of this AI apprehension, the implementation of agentless solutions opens up the insurance industry for more growth and change. It allows companies like Transamerica and MetLife to have incubators and investment arms, which allows them to innovate in preparation for incoming “market killer” competitors. This even allows insurers, like Principal and Assurity, to raise their coverage maximums as high as $1 million without medical exams. Just like in any other industry, it may take time for consumers to get used to the idea of using AI for insurance buying.

Where would you feel most confident buying a life insurance policy?

- 78% of respondents said they would feel most confident buying life insurance from a local agent versus a big box retailer or online agency.

- For Gen Z respondents, outside of a local agent, Costco, Walmart, and Amazon were more popular choices than online agencies, the overall second choice.

The popularity of local agents in this question illustrates consumer apprehension toward agentless solutions. Despite this, many insurers are still pursuing agentless solutions, cutting out many of the human elements of their processes in favor of convenience and cost-cutting.

Though they rank relatively low in our survey results, Costco, Amazon, and Walmart have all entered the insurance industry in one way or another in recent years. They stand to drastically change the way everyone in the insurance industry does business, which is why some consider them “market killers.”

To add even more credence to the potential of these “market killers,” for Gen Z respondents (aged 18-24), Costco, Walmart, and Amazon were all more popular options than an online agency, which was the overall second choice. As they were the only demographic who responded like this and will soon start buying insurance, this is clear evidence for why these established retailers and brands stand to be key forces in the insurance world moving forward.

Insurancy surveyed 1047 people in the United States ages 18 - 55.