What are the Types of Buy-Sell Agreements?

Buy-sell agreements can take different forms, but the two typical structures are cross-purchase plans and entity redemption plans, with a hybrid version also available as a third possible option.

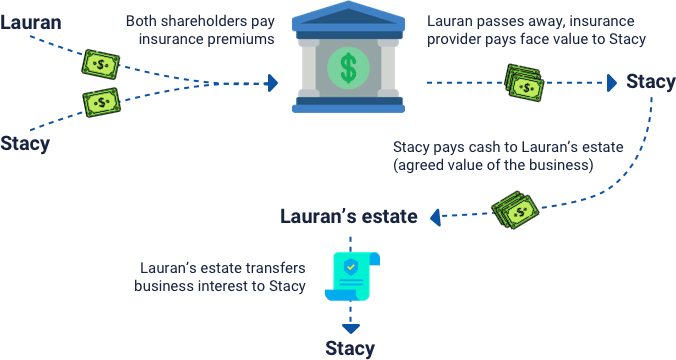

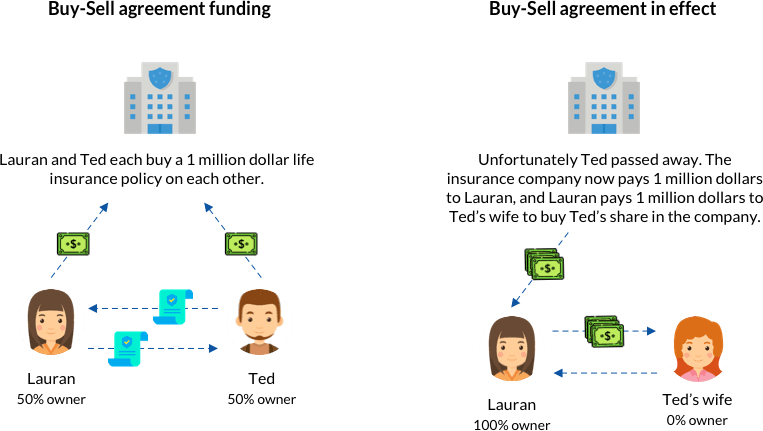

Cross Purchase Plan

In a cross purchase plan, each owner purchases a life insurance policy on the other owner or owners. Each owner pays the annual premiums on the policy they own and each is the beneficiary of the policy. When an owner dies, the surviving owners use the death benefit to purchase the deceased owner’s share of the business. If there are a large number of owners of the business, multiple policies must be purchased by each owner.

Example

In the following Cross Purchase Plan example, the business is valued at 2 million dollars, and has 2 owners, Lauran and Ted. Each owner holds 50% of the company.

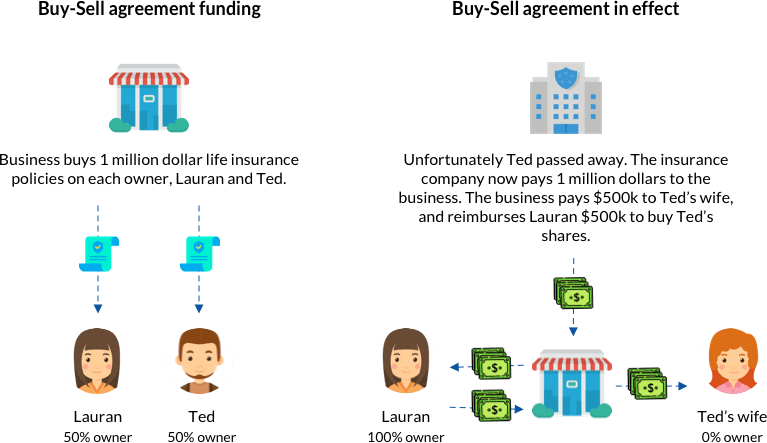

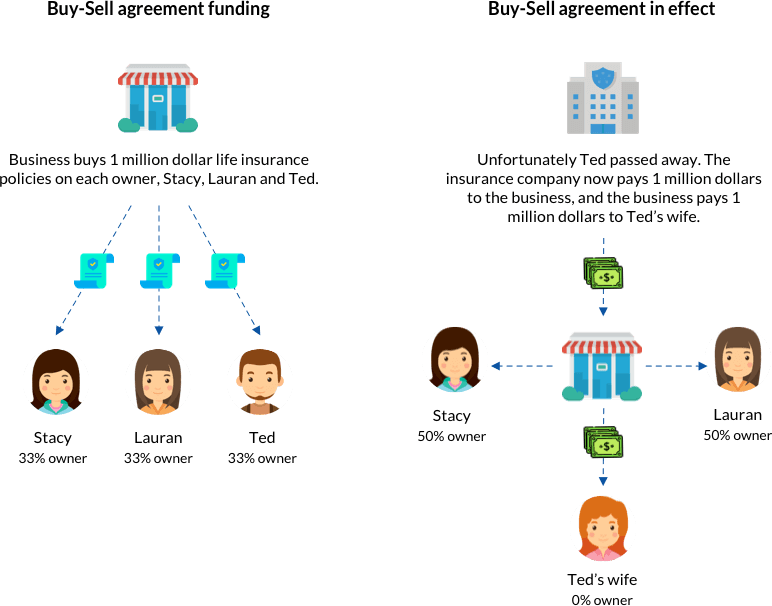

Entity Redemption Plan

In an entity redemption plan, each owner has an arrangement with the business for the sale of their respective interests to the business. The business purchases separate life insurance policies on the lives of the owners. The business pays the premiums. And the business is the owner and beneficiary of the policy. When an owner dies, his or her share of company stock will pass to his or her heirs or estate, and the company may purchase them with the proceeds from the life insurance policy.

Example

In the following Entity Redemption Plan example, the business is valued at 3 million dollars, and has 3 owners, Stacy, Lauran and Ted. Each owner holds 33% of the company.

Hybrid Plan

A hybrid plan, as you might have guessed, combines the first two types of buy–sell agreements: cross purchase and entity redemption. Typically, the owner is required to offer his or her interest to the entity. If the entity declines or cannot make the purchase, however, other co-owners or partners can purchase the shares. This type of arrangement may also allow certain employees, like longtime company officials, to purchase the interest.

Example

In the following Hybrid Plan example, the business is valued at 1 million dollars, and has 2 owners, Lauran and Ted. Each owner holds 50% of the company.