Quick answer

Final expense life insurance is a small whole life insurance policy, typically $2,000 to $50,000, designed to cover funeral costs, end-of-life medical bills, and small outstanding debts. Most final expense policies have no medical exam, simplified-issue underwriting, and approval within 24 to 48 hours. Coverage is most commonly purchased by ages 45 to 89, and the policy remains in force for life as long as premiums are paid.

Best Final Expense Life Insurance Companies

The carriers below are the top-rated final expense providers we represent. Each is A.M. Best A or higher. We have removed Great Western Life Insurance (exited new final expense market 2024-08-31) and American National (exited new life insurance entirely in 2023) per the Insurancy Playbook carrier status tracker.

| Company | Recommendation | Rating | Best for | Quote |

|---|---|---|---|---|

|

Recommended. Living Promise final expense. Coverage $2,000 to $40,000. Ages 45 to 85. Day-one full benefit on level plan. Apply with an agent. |

★★★★★ Mutual of Omaha Review |

Best overall final expense carrier. Day-one full benefit available for healthy applicants. | Go |

|

Recommended. Aetna Accendo whole life. Coverage $2,000 to $50,000. Ages 45 to 89. Strong rate classes for tobacco users. |

★★★★★ A.M. Best A rated |

Best final expense for tobacco users and applicants with moderate health conditions. | Go |

|

Recommended. PlanRight Whole Life. Coverage $5,000 to $35,000. Ages 50 to 85. Member benefits included. |

★★★★★ Foresters Review |

Best final expense with fraternal member benefits (orphan benefit, scholarship benefit, family health benefit). | Go |

|

Recommended. Guaranteed Acceptance Whole Life. Coverage $5,000 to $25,000. Ages 50 to 80. No health questions. Modified-benefit waiting period. |

★★★★☆ Gerber Life Review |

Best guaranteed-acceptance final expense for applicants who would not qualify for simplified-issue. | Go |

|

Recommended. Guaranteed Issue Whole Life. Coverage $5,000 to $25,000. Ages 50 to 80. No health questions. 2-year modified-benefit period. |

★★★★★ Corebridge Review |

Best alternative guaranteed-acceptance carrier for applicants declined by other final expense carriers. | Go |

Policy Types

Final expense life insurance comes in six different types. Each type has its own structure and pricing. Generally, the healthier the applicant is, the more benefits the policy will include, and the more affordable the policy will be.

We’ll talk about each type of final expense in depth below:

- Level benefit

- Graded benefit

- Modified benefit

- Guaranteed acceptance

- Funeral Home

- Group insurance

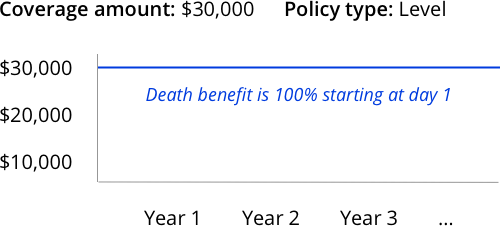

Level Whole Life Policies With Immediate Benefit

A level policy is the most basic and straightforward of the final expense policies. Level policies are issued to applicants who are in good health, with any health issues having been controlled for at least three years. The full amount of the policy will be in effect the day the application is approved. When the insured person dies, the named beneficiaries can receive the full death benefit right away.

Specifications of level whole life policies

- Full coverage from day 1

Unlike graded or modified benefit policies, an immediate benefit policy will provide 100% of the death benefit starting on day 1. - Best-priced final expense plan

Out of the six types of final expense policies, an immediate benefit plan has the best price and offers the best benefits. - Offers a higher coverage amount

Level whole life policies can be purchased for $2,500 to $100,000, depending on the insurance provider.

What do you need to qualify for an immediate benefit/level whole life policy?

- No major medical diagnosis or treatment in the past three years, including:

heart attack, internal cancer, leukemia, respiratory disorder, diabetes diagnosed before age 40, stroke, COPD, Crohn’s disease, cerebral palsy, and MS - No history of:

congestive heart failure, cardiomyopathy, Parkinson’s disease, paralysis, amputation or dependency on a wheelchair, dialysis, Alzheimer’s disease, ALS, AIDS, HIV, or current hospitalization - All medical conditions are well-controlled.

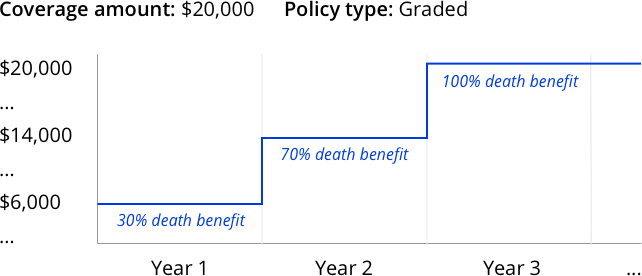

Graded Benefit Policies

Depending on the insurance company chosen, applicants can often qualify for a graded policy if they have not had any major illnesses in the past 24 months.

For example, a graded plan might be right for someone with Parkinson’s disease or some other medically manageable disease. If a non-accidental death occurs within a two-year time frame, the policy will only pay a percentage of the total death benefit. During the third year and beyond, the entire death benefit will be paid.

Specifications of graded benefit policies

- Graded death benefit

Unlike immediate benefit policies, a graded death benefit policy will pay 30% of the coverage amount to the beneficiaries during the first year. The second year, the death benefit is increased to 70%. At the start of the third year, the death benefit will become 100%. - Accidental death rider

If the cause of death is due to an accident, the beneficiaries will receive 100% of the death benefit, starting on day 1. - Return of premium + 10% in the case of suicide

If the cause of death is due to suicide, the beneficiaries will receive any paid premiums plus 10%.

What do you need to qualify for a graded whole life policy?

- No major medical diagnosis or treatment in the past three years, including:

heart attack, internal cancer, leukemia, respiratory disorder, diabetes diagnosed before age 40, stroke, COPD, Crohn’s disease, cerebral palsy, and MS - No history of:

dialysis, Alzheimer’s disease, ALS, AIDS, HIV, or current hospitalization - All medical conditions are well-controlled.

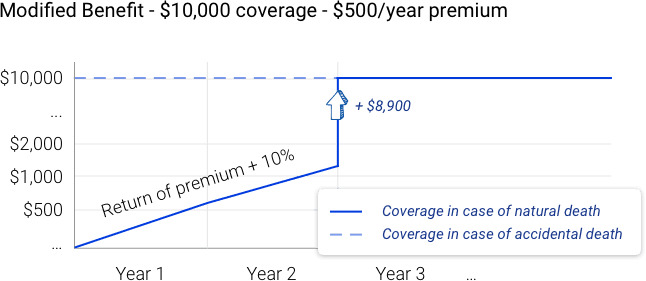

Modified Benefit Policies

A modified policy is very similar to a graded policy except it involves a serious illness, such as cancer, instead of a more manageable ailment. Modified policy benefits usually have a two-year waiting period before the entire death benefit can be paid to a beneficiary.

If a non-accidental death occurs before that two-year time frame, the policy will only pay a return of the paid premiums plus a small percentage of the total death benefit. During the third year and beyond, however, the entire death benefit will be paid.

Specifications of modified benefit policies

- Graded death benefit

During the first two years of the policy, the beneficiaries will receive any paid premiums plus 10%. At the start of the third year of the policy, the beneficiaries will receive 100% of the death benefit. - Accidental death rider

If the cause of death is due to an accident, the beneficiaries will receive 100% of the death benefit, starting on day 1. - Return of premium + 10% in the case of suicide

If the cause of death is due to suicide, the beneficiaries will receive any paid premiums plus 10%. - Coverage amounts of $1,000 to $40,000

What do you need to qualify for a modified benefit whole life policy?

- No major medical diagnosis or treatment in the past three years, including:

heart attack, internal cancer, leukemia, respiratory disorder, diabetes diagnosed before age 40, stroke, COPD, Crohn’s disease, cerebral palsy, and MS - No history of:

dialysis, Alzheimer’s disease, ALS, AIDS, HIV, or current hospitalization - All medical conditions are well-controlled.

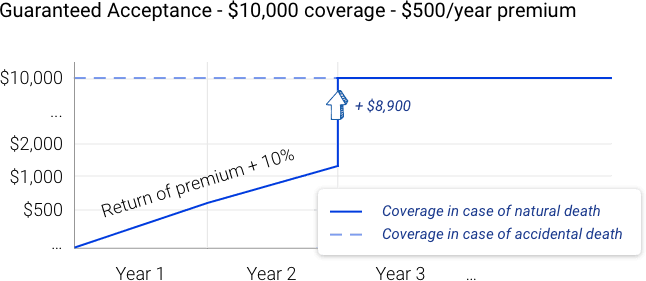

Guaranteed Acceptance Policies

A guaranteed issue policy is a policy with no health questions. There’s a two-year waiting period before the entire death benefit can be paid to a beneficiary.

In years 1 and 2, the benefit is the return of all the money paid thus far plus 10%. This protects insurance companies in cases where the person who purchases the policy already has a terminal diagnosis or is in hospice. For accidental death, the full benefit amount is paid to beneficiaries in years 1 and 2.

In year 3, the full benefit amount is paid to beneficiaries.

Specifications of guaranteed acceptance policies

- Graded death benefit

During the first two years of the policy, the beneficiaries will receive any paid premiums plus 10%. At the start of the third year of the policy, the beneficiaries will receive 100% of the death benefit. - Accidental death rider

If the cause of death is due to an accident, the beneficiaries will receive 100% of the death benefit, starting on day 1. - Return of premium + 10% in the case of suicide

If the cause of death is due to suicide, the beneficiaries will receive any paid premiums plus 10%. - Coverage amounts of $1,000 to $40,000

What do you need to qualify for a guaranteed acceptance whole life policy?

- There are no health questions. Acceptance is guaranteed.

Funeral Insurance

A pre-need funeral policy is purchased directly from a funeral home, and the funeral home is named as the beneficiary. The purpose is to pay for one’s funeral in advance. The policy covers the cost of funeral home services, a casket, burial fees, and memorial services.

The negatives: This is more like a layaway plan than a life insurance policy. These plans are offered as single-pay, 1-year, 5-year, and 10-year payment options. Once a plan is chosen, it’s locked in and difficult (or impossible) to change.

The positives: The positives: Once the plan is in place, there is no hassle or worry about needing to plan for a funeral at the last minute. And, the prices are set ahead of time.

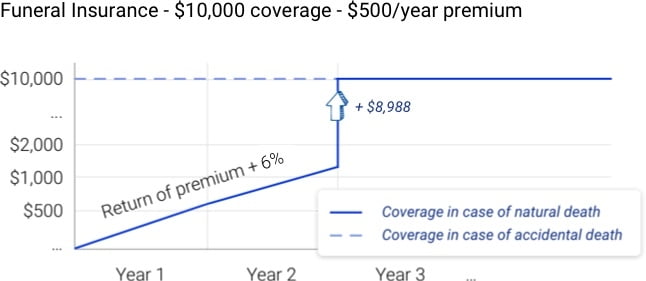

Specifications of funeral insurance policies

- Graded death benefit

During the first two years of the policy, the beneficiaries will receive any paid premiums plus 6%. At the start of the third year of the policy, the beneficiaries will receive 100% of the death benefit. - Accidental death rider

If the cause of death is due to an accident, the funeral home will receive 100% of the death benefit, starting on day 1. - Return of premium + 6% in the case of suicide

If the cause of death is due to suicide, the funeral home will receive any paid premiums, plus 10%. - The funeral home is the beneficiary

- Coverage amounts of $1,000 to $20,000

What do you need to qualify for a funeral insurance policy?

- There is no health qualification. Acceptance is guaranteed.

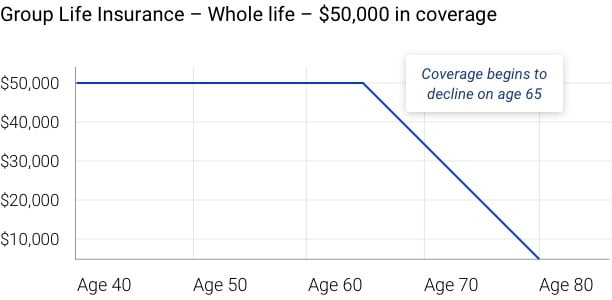

Group Life Insurance

Group life insurance is a type of policy that is provided by an employer, an association, or an organization. Each group has its own requirements for becoming a member.

Each group or association has different products. The products are issued by an insurance company, but the group is the master policyholder. This means that instead of the insurance company issuing each person an individual policy, everyone named on the policy receives a certificate of insurance.

Service for the policy is provided by the plan administrator rather than the insurance company directly.

Group life insurance is available to all ages, and there are very few health questions, if any, to qualify. Coverage amounts start at $10,000. Term and whole life policies may be available, depending on the group.

Specifications of group insurance policies

- Full coverage from day 1

Unlike graded or modified benefit policies, an immediate benefit policy will provide 100% of the death benefit starting on day 1. - Just a few health questions to apply

- Issued a certificate of insurance rather than a full policy

- May be canceled if the group terminates

- Coverage amounts of $10,000 to $75,000

What do you need to qualify for a group insurance policy?

- Membership requirements depend on the group.

Ready to compare final expense quotes? Start here